COVID-19 has impacted us all in recent weeks. At Edge we have put plans in place that have allowed us to provide all services our clients require without disruption.

We are working diligently to understand the impacts COVID-19 could have on the energy markets in the short and longer term. As more information comes to light, we will provide further updates on the impacts to the market and our clients.

As we are only a few weeks into this pandemic we will try and provide an understanding of the impact COVID-19 could have on the market.

Oxford economics, a team of 250 economists, has recently published a paper providing a high-level update on the impact of the pandemic on the world economy. Their initial work predicts a short, sharp recession to the global economy with major national economies going into deep recession during the first half of 2020. It is modelled that over the full year global growth will drop to zero.

Oxford economics are predicting, based on historic experience, a strong bounce back in activity once social distancing measures are relaxed. It is forecast that businesses that can get through the first half of 2020 should be prepared for a strong second half of 2020, with global growth forecast above 4%.

Overseas experience

As China was the first country to close-down as a result of COVID-19 we can learn from their recent energy experience and translate it into the Australian market.

In January and February energy production dropped significantly with thermal power dropping 8.9%, hydro dropping 11.9% and nuclear and wind dropping to a lesser extent at 2.2% and 0.2% respectively. On the flip side Solar generation increase by 12%.

Early indications are that thermal and hydro station dropped production the most due to reduced staffing level causing lower operational hours. Renewables were impacted the least due to their non-dispatchability.

It is estimated that during the height of the Chinese lockdown period over the 27 days, demand decreased by 16%.

At Home in Australia

Generation

Large generation portfolio’s including the likes of Stanwell and AGL have publicly acknowledged they have put plans in place to ensure generation meets demand, this includes stockpiling coal to ensure security of fuel supply. Smaller generators on the other hand may not have the staff to guarantee operation of their units over the long term due to illness.

Energy Price Impacts

With the additional impact of lower energy demand in Asian countries such as China, Australia’s liquefied natural gas demand significantly reduced, resulting in excess domestic gas supply particularly on the east coast of Australia. Although majority of the LNG facilities on the east coast reside in QLD, we have seen an increase in gas generation and a decrease in bid prices in regions more dependent on and abundant with gas-fired generation, such as South Australia. We are seeing approximately 600 MW more of gas-fired generation in March 2020, compared to March 2019, bid in at prices below $50/MWh. Assisting this is the collapse in natural gas prices in the Adelaide Short-term Trading Market, which has traded at the mid to high $5/GJ range for March 2020, compared to the significantly higher price range of $10 – $11/GJ we witnessed back in March 2019. Both of these variables are introducing cheaper supply in the energy markets both for heating (in homes) and electricity generation. With interconnection remaining relatively unconstrained this is resulting in lower prices across all NEM regions.

AEMO

AEMO has put in place its pandemic response plan so the market operator can continue to operate the NEM and WEM efficiently and safely. Key actions in the pandemic plan include limiting contact with key staff such as control room and other business critical staff.

Demand

Following the initial breakout of COVID-19 in Australia and the early shutdown of some businesses, demand fell by about 600MW in NSW or about 8% of average demand. This was reflective of all states. Over the recent week the steep reductions in demand experienced at the start of COVID-19 have flattened out as a result of two possible reasons. In some regions such as Victoria, demand has increased. The first reason for this change in demand is consumption has moved from businesses to individual homes. Across Australia average demand is currently only 7% below last month’s average. The demand change is also attributed to seasonal change which has resulted in a reduction in load associated with cooling.

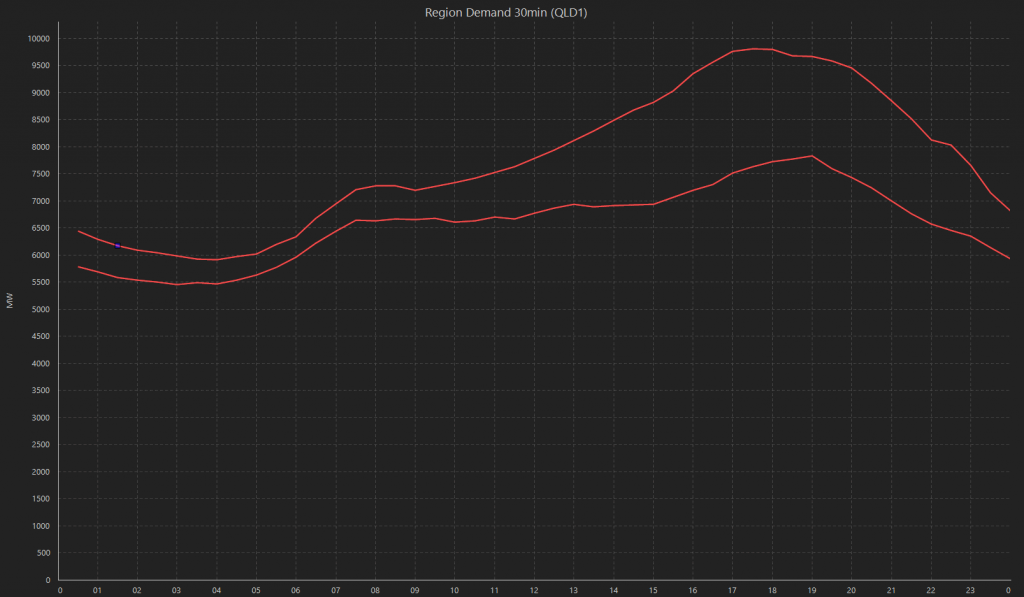

Change in demand – daily profile

The chart below illustrates the change in demand across the day and compares a summer profile and a transition to an autumn profile. The top line is early February with the bottom-line showing demand from Monday the 23rd March.

The chart shows morning peak has reduced slightly however the demand over the evening peak has dropped significantly.

Impact of large users

It is expected that large users would be impacted significantly by the virus however this does not appear to be the case. With parts of the world such as South Africa shutting down mines and industry following government direction the supply / demand balance is falling in the favour of Australia. Add to this the favourable exchange rates, the export potential of commodities from Australia remains strong. The Australian mining industry is also designated as an ‘Essential Service’ so at this stage they are sheltered from future lock downs. This positive news for the mining sector which will benefit mining rich states with demand expected to reduce to a lesser extent than other states.

Renewables

If the trends overseas are reflected in Australia the current installed capacity of renewable generation will continue to operate at strong levels providing staffing is available to operate and control the assets.

There will be a likely slowdown in the development of renewable projects as a result of the restrictions on travel, meetings and specialist staff available for construction, connection, commissioning and final approvals.

This slowdown will impact the future mix of generation assets across Australia, the current trend in carbon emission reductions and the supply and price of environmental products.

LGCs

Edge has modelled the impact of a 10% reduction in demand with a business as usual generation profile for large scale renewable generators to understand the impact this downturn may have on LGC supply and price.

The 10% reduction in demand could reduce the RPP percentage by 0.32%. The likely effect of a reduced percentage and business as usual renewable production will be surplus LGCs in the short term and reduced prices for LGCs.

STCs

With the downturn of the economy it is expected that less roof top solar will be installed resulting in a reduction in the current surplus of certificates carried forward since 2017. The reduction is expected to reduce the STP below 20%.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.