On the 26 March 2020, the energy market bodies including the Australian Energy Market Commission (AEMC), Australian Energy Market Operator (AEMO) and the Australian Energy Regulator (AER) wrote a letter to the Australian Federal Government’s Energy Minister, Angus Taylor which advised and sought for the consideration to consider a longer implementation time-frame for the market’s transition to the 5 minute settlement regime which was pegged to begin on 1 July 2021.

The Market bodies have stipulated the reasoning for this is due to the vast impacts to industry and the workforce that have occurred due to the COVID-19 outbreak. The letter to Mr Taylor proposes delaying the start date of 5 minute settlement by 12 months so industry can defer further/remaining expenses associated with preparing for 5 minute settlement.

It also states that AEMO will still work to the same deadline, albeit 12 months would provide AEMO with extra time to ensure 5 minute scheduling and dispatching engines are sound at least in a development environment. As yet we do not know if the 5 minute settlement will get the go ahead to be delayed, with market bodies still reaching out to market participants to advise as to whether this will be advantageous or not.

The impact of a 5 minute settlement delay to the market will be impact all participants and investment decisions, there are some calling out this only extends coal-fired generation’s life-span, but if you have been watching the futures prices and spot prices of late, coal-fired generation is already in a world of hurt with no doubt a lot of questions being raised about the remaining lifespan of some coal plant in both QLD and NSW. Should 5 minute settlement be delayed by 12 months, there is the likelihood we see the slide of investment in some fast start plant, such as new batteries and hydro.

Gas-fired generators who have not re-tuned/upgraded their synchronising and start time to less than 5 minutes will still have the 30 minute settlement price to fall back on at least for another 12 months and be able to capture any value the 30 minute average settlement price may represent. The flip side of 5 minute settlement is that it would be very good for renewable generation as it would make the thermal plat operators reassess their operating philosophies with gas likely more removed from the market, and propping up the price.

The 2021/2022 financial year was likely to be a more costly financial year given the introduction of 5 minute settlement, which would effectively mean a vast majority of gas plant would not be able to curb price spikes as effectively under the new settlement regime, resulting in a change to their operating philosophy, however both the impacts of COVID-19 an the recent oil price collapse has significantly changed this stance.

Unfortunately, there is no real way to know how much of an impact globally it will have, and how long the impacts of COVID-19 will last. Similarly, with Saudi-Arabia and Russia both engaged in a price/supply war over Oil (two of the largest producers of oil) it is all hard to depict how long the extremely cheap domestic gas prices will last, particularly with investment decisions in new domestic gas likely put on hold.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

COVID-19 has impacted us all in recent weeks. At Edge we

have put plans in place that have allowed us to provide all services our clients

require without disruption.

We are working diligently to understand the impacts COVID-19

could have on the energy markets in the short and longer term. As more

information comes to light, we will provide further updates on the impacts to

the market and our clients.

As we are only a few weeks into this pandemic we will try

and provide an understanding of the impact COVID-19 could have on the market.

Oxford economics, a team of 250 economists, has recently

published a paper providing a high-level update on the impact of the pandemic

on the world economy. Their initial work predicts a short, sharp recession to

the global economy with major national economies going into deep recession

during the first half of 2020. It is modelled that over the full year global

growth will drop to zero.

Oxford economics are predicting, based on historic experience,

a strong bounce back in activity once social distancing measures are relaxed.

It is forecast that businesses that can get through the first half of 2020

should be prepared for a strong second half of 2020, with global growth forecast

above 4%.

Overseas experience

As China was the first country to close-down as a result of

COVID-19 we can learn from their recent energy experience and translate it into

the Australian market.

In January and February energy production dropped

significantly with thermal power dropping 8.9%, hydro dropping 11.9% and nuclear

and wind dropping to a lesser extent at 2.2% and 0.2% respectively. On the flip

side Solar generation increase by 12%.

Early indications are that thermal and hydro station dropped

production the most due to reduced staffing level causing lower operational

hours. Renewables were impacted the least due to their non-dispatchability.

It is estimated that during the height of the Chinese

lockdown period over the 27 days, demand decreased by 16%.

At Home in Australia

Generation

Large generation portfolio’s including the likes of Stanwell

and AGL have publicly acknowledged they have put plans in place to ensure

generation meets demand, this includes stockpiling coal to ensure security of

fuel supply. Smaller generators on the other hand may not have the staff to

guarantee operation of their units over the long term due to illness.

Energy Price Impacts

With the additional impact of lower energy demand in Asian countries such as China, Australia’s liquefied natural gas demand significantly reduced, resulting in excess domestic gas supply particularly on the east coast of Australia. Although majority of the LNG facilities on the east coast reside in QLD, we have seen an increase in gas generation and a decrease in bid prices in regions more dependent on and abundant with gas-fired generation, such as South Australia. We are seeing approximately 600 MW more of gas-fired generation in March 2020, compared to March 2019, bid in at prices below $50/MWh. Assisting this is the collapse in natural gas prices in the Adelaide Short-term Trading Market, which has traded at the mid to high $5/GJ range for March 2020, compared to the significantly higher price range of $10 – $11/GJ we witnessed back in March 2019. Both of these variables are introducing cheaper supply in the energy markets both for heating (in homes) and electricity generation. With interconnection remaining relatively unconstrained this is resulting in lower prices across all NEM regions.

AEMO

AEMO has put in place its pandemic response plan so the

market operator can continue to operate the NEM and WEM efficiently and safely.

Key actions in the pandemic plan include limiting contact with key staff such

as control room and other business critical staff.

Demand

Following the initial breakout of COVID-19 in Australia and

the early shutdown of some businesses, demand fell by about 600MW in NSW or

about 8% of average demand. This was reflective of all states. Over the recent

week the steep reductions in demand experienced at the start of COVID-19 have

flattened out as a result of two possible reasons. In some regions such as

Victoria, demand has increased. The first reason for this change in demand is

consumption has moved from businesses to individual homes. Across Australia average

demand is currently only 7% below last month’s average. The demand change is

also attributed to seasonal change which has resulted in a reduction in load

associated with cooling.

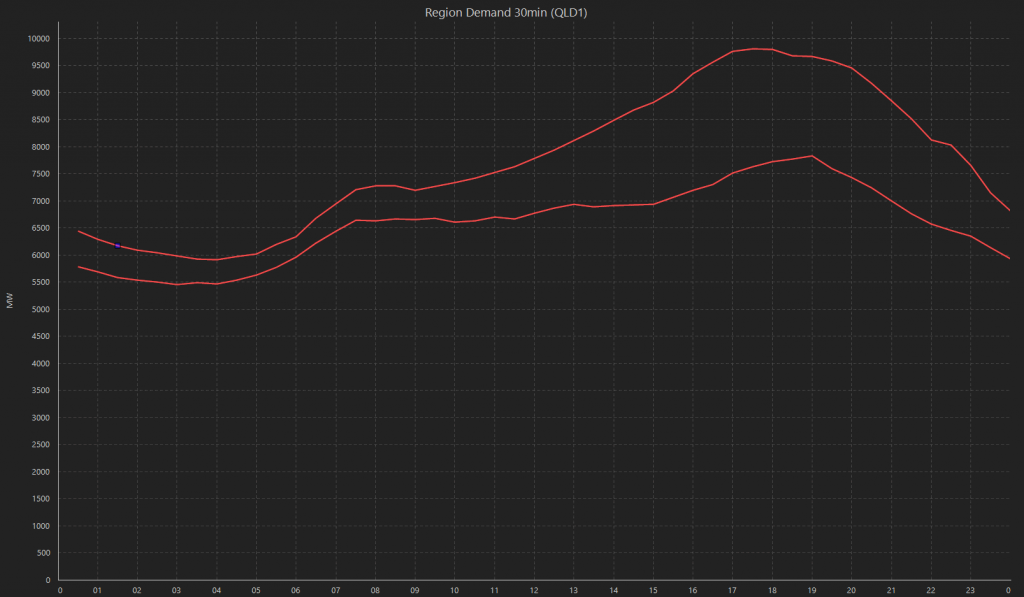

Change in demand – daily profile

The chart below illustrates the change in demand across the

day and compares a summer profile and a transition to an autumn profile. The

top line is early February with the bottom-line showing demand from Monday the

23rd March.

Source: AEMO 2020

The chart shows morning peak has reduced slightly however the demand over the evening peak has dropped significantly.

Impact of large users

It is expected that large users would be impacted significantly

by the virus however this does not appear to be the case. With parts of the

world such as South Africa shutting down mines and industry following

government direction the supply / demand balance is falling in the favour of

Australia. Add to this the favourable exchange rates, the export potential of

commodities from Australia remains strong. The Australian mining industry is

also designated as an ‘Essential Service’ so at this stage they are sheltered

from future lock downs. This positive news for the mining sector which will

benefit mining rich states with demand expected to reduce to a lesser extent

than other states.

Renewables

If the trends overseas are reflected in Australia the

current installed capacity of renewable generation will continue to operate at

strong levels providing staffing is available to operate and control the

assets.

There will be a likely slowdown in the development of

renewable projects as a result of the restrictions on travel, meetings and

specialist staff available for construction, connection, commissioning and

final approvals.

This slowdown will impact the future mix of generation

assets across Australia, the current trend in carbon emission reductions and

the supply and price of environmental products.

LGCs

Edge has modelled the impact of a 10% reduction in demand

with a business as usual generation profile for large scale renewable generators

to understand the impact this downturn may have on LGC supply and price.

The 10% reduction in demand could reduce the RPP percentage

by 0.32%. The likely effect of a reduced percentage and business as usual

renewable production will be surplus LGCs in the short term and reduced prices

for LGCs.

STCs

With the downturn of the economy it is expected that less

roof top solar will be installed resulting in a reduction in the current

surplus of certificates carried forward since 2017. The reduction is expected

to reduce the STP below 20%.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

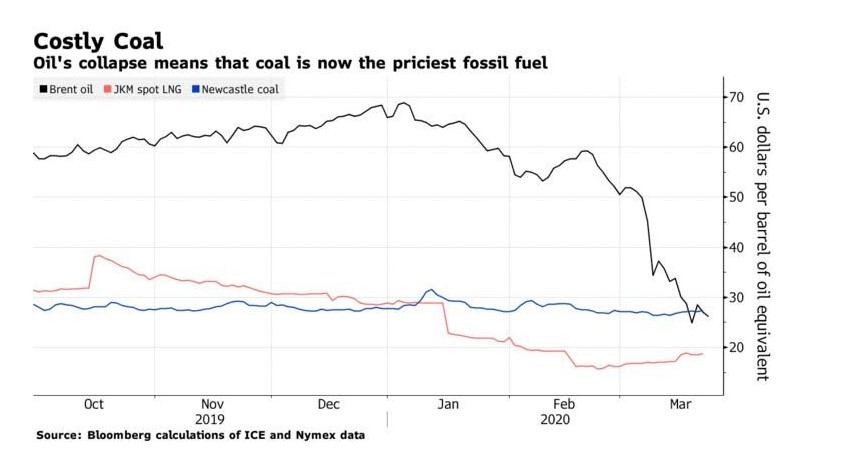

We have all seen recently the impact that COVID-19 has had on global markets, in terms of stock prices, equity markets and of commodity markets.

Exacerbating this was the poor timing of Saudi Arabia and Russia’s spat over oil prices and both choosing to disagree on production levels, the disagreement lead to Saudi Arabia choosing to flood the oil markets with supply inevitably driving oil prices down significantly, with the WTI Crude Oil index reaching its lowest point in the last 5 plus years or so, trading in the low to mid $USD 20/barrel, also impacting the Brent Crude Oil index, which fell to its lowest point in the last 5 years or so to prices of the high $USD 20/barrel. Both events have lead to something quite astounding, with Bloomberg Green on the 23rd of March 2020 calculating that coal was officially the world’s most expensive fossil fuel.

Source: Bloomberg Green – Bloomberg 2020

This does not come as a huge surprise when the oil price has tanked off the back of a trade war between Saudi Araba and Russia, two of the largest producers of oil in the world. Additionally, international gas prices have also tanked with majority of long-term gas deals linked to an oil price index (likely Brent Crude) and the Japan Korea Marker – a major LNG (liquefied natural gas) index for Asia also falling with a supply glut due to reductions in demand from some of the largest demand centres such as China who went into a full lockdown earlier this year due to COVID-19.

According to Bloomberg calculations (Bloomberg 2020), the significant fall from grace in oil prices has meant that global crude benchmark is now priced below the Australian Newcastle coal index, which sat at $66.85 a metric ton on ICE Futures Europe on the 23/03, equivalent to $27.36 per barrel of oil with Brent futures that day ending at $26.98 per barrel.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The South Australian (SA) region has been separated from the remainder of the NEM regions due to the destruction of the main alternating-current (AC) interconnector between SA and Victoria (VIC).

What occurred:

On the 31st of January 2020 during wild storms that lashed eastern SA, western VIC, the 500kV main (AC) interconnection cable running through southwestern VIC was disconnected due to transmissions towers east of Heywood (Victoria) and west of Geelong (Victoria) collapsing in damaging storms and extremely strong winds.

When this occurred,

Interconnection flows quickly swung from exporting MW’s into VIC, to importing MW’s into SA.

Alcoa’s Portland aluminium smelter tripped which only exacerbated the problem,

A handful of wind farms were cut off from the market including McCarthur Wind Farm (420 MW) in Victoria, and the three Lake Bonney Projects in South Australian (~278.5 MW)

What does this mean:

Basically SA has been left to fend for itself, cut-off from the rest of the NEM

All MW’s (majority of all, with the small Murraylink direct-current interconnector still available) and frequency control services must be sourced from SA, locally.

Currently all SA generators are running hard and optimising portfolio’s for frequency control services (FCAS) prices rather than regional reference prices (spot price)

Additionally, a vast majority of gas-fired generation units including, Osbourne GT, Pelican Point, Torrens Island A and B units have and continue to receive market intervention notices from AEMO requiring them to be online

This is adding to the oversupply in the region with wind generation quite strong for this time of the year,

Not to mention, the wind generation, being a variable generation type, is not helping from a forecast perspective for AEMO, adding to the FCAS costs and requirements in the SA region.

Solution:

AEMO have indicatively provided a two week return time off the back of AusNet’s (interconnector owner) initial assessment and action plan to fix the interconnector.

AusNet’s solution is to construct temporary interconnection with power poles and lines to have arrived on site yesterday (03/02/2020).

Current weather forecast and impact on spot price:

Currently temperatures are set to be relatively mild for an SA summer at this stage.

However, temperatures are expected to reach the late 20’s and early 30’s towards the end of the week, historically, temperatures at these levels have encouraged higher demand and the need for imports from VIC, which will not be possible with the largest interconnector between the two regions out of action.

Although we are seeing some extreme lows in spot price, there is the possibility we could see some extreme highs. It is dependent on:

AEMO’s intervention in the market with AEMO issuing FCAS targets to participants in the realm of $300/MWh for raise and lower services (due to the inability to source FCAS from outside of SA), and

Generators potentially looking to spike spot prices or increase the spot price with no doubt, gas generator running costs no doubt increasing every MWh the interconnector is out of action.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

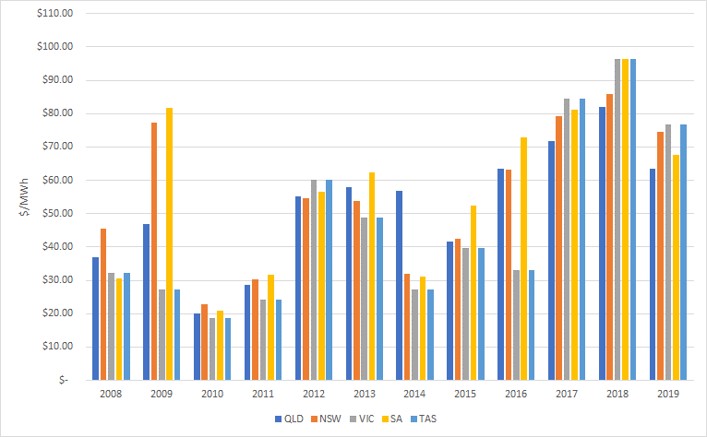

Electricity spot prices in Q419 (October to December) were softer than the prior two Q4’s in Calendar Year 2017 and 2018. Q419 prices continued to be relatively mild following on from Q319’s performance. We did start to see a little more volatility creep into the spot prices towards the end of the year mainly due the bushfire disaster around the NEM and also with heatwave conditions starting to form.

Figure 1: Historical prices for Spring/Summer

(Source: AEMO)

Throughout October and November 2019, we saw milder temperatures and above average wind generation in both VIC and SA with the Bureau of Meteorology (BoM) indicating that a longer than expected Negative SAM (Southern Annular Mode) event was resulting in cooler than expected temperatures and stronger and more frequent westerly winds which was only helping drive solid wind generation levels in the southern NEM regions. As a result, both VIC and SA experienced multiple negatively priced half hours during the daylight hours, with interconnector constraints really dragging down SA’s spot price causing an oversupply in the region; however, cooler temperatures in VIC drove peakier morning and evening peak prices, keeping its spot price for October at least relatively elevated.

SA did however receive a taste of Summer peak pricing and demand, with extreme temperatures leading to a max of 44.8 degrees in Adelaide 19/12. Overnight temperatures on the 19/12 were above 33 degrees in Adelaide at 7pm encouraging the use of air-conditioning and leading to a ramp spike in demand which encouraged a full hour of VoLL (value of loss load) pricing at $14,700/MWh.

Assisting VIC’s peak pricing was the continued downtime of AGL’s Loy Yang A2 unit and Origin’s Mortlake Unit 2 with Mortlake making a return in December 2019, and Loy Yang A2 back for Christmas, offline again shortly after, then offline again for the remainder of the 2019 calendar year. Assisting VIC’s spot price for the quarter was a surge in price in Tasmania for October 2019. With Basslink offline the entire month of September 2019, it would seem both the Basslink operator and Hydro Tas had to play catch-up, keeping the spot price elevated for majority of the October 2019 month, allowing Tas to come away with the highest spot price for October 2019 of all NEM regions.

QLD experienced relatively mild demand and temperatures for the Spring months, and with an already oversupplied market, the introduction of Clean Co and their remit from the QLD government to run down spot prices, and Shell’s take-over of ERM, challenging the market dynamics, resulted in softer than expected spot prices for October and November 2019.

NSW had an interesting run over Q419, sharing in the spoils of the elevated spot prices in VIC and Tas in October 2019 with multiple baseload generators out of action for maintenance, to then dealing with the bushfire crisis in late November through December 2019, resulting in demand losses and cutting generation off from the NEM. Snowy Hydro’s Upper Tumut Pumped Hydro and Tumut 3 Hydro units dispatched frequently throughout the quarter, particularly in December 2019 also choosing to spill at relatively weak spot prices around the $70/MWh mark. I do wonder if we will continue to see Snowy spill at such weak spot prices with water levels at lake Eucumbene starting to plateau at ~30% after a steady incline throughout the last Quarter.

Obviously, impacting all regions in December 2019 was the holiday season shutdown of workplaces and schools, driving lower demand throughout the month.

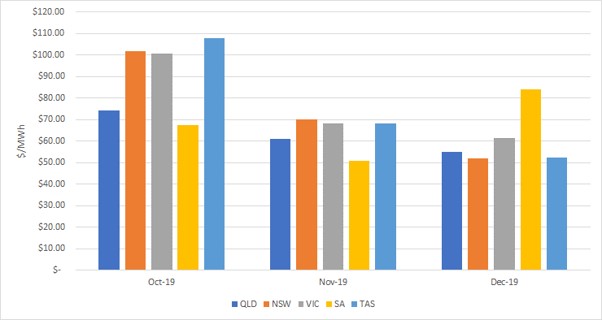

Figure 2: Average monthly spot prices in the NEM

(Source: AEMO)

Friday the 22nd of November saw The Council of Australian Government’s Energy Council meet in Perth to discuss the current and future state of Australia’s Energy network. The key focus for COAG’s energy council was energy security and reliability focussing on Summer 2020 in the near-term and potential changes required for future state surrounding those two variables and of course how to make energy more affordable. Additionally to this, the COAG Energy Council also threw its support behind a National Hydrogen Strategy as laid out by Australia’s chief scientist, Dr. Alan Finkel. AEMO presented to the council outlining how they have prepared for Summer 2020, however COAG’s Energy Council has put forward a call for the Energy Security Board to reassess and to re-jig the current reliability standard (a measure used to ensure enough spare capacity is in the grid to cope with extreme demand days).

Fed Energy Minister Angus Taylor was seeking tougher reliability standards with the rapid influx of renewable generation that now makes up a significant chunk of Australian energy supply, whilst Victorian Energy Minister Lily D’Ambrosio wants tougher standards to deal with the ailing coal-fired generators in her region; either way both were seeking the same result.

There is however the push for higher reliability standards will lead to further ‘gold-plating’ of the network and inevitably higher energy prices for consumers. Probably one of the more surprising outcomes of the COAG Energy Council meeting was the vast support for a National Hydrogen Strategy as put forward by Dr. Alan Finkel and supported by Angus Taylor on the 22nd of November. $370 million dollars will be committed by the Clean Energy Finance Corp (CEFC) and the Australian Renewable Energy Agency (ARENA) to kick start and bankroll “electrolyser” projects, which can convert electricity to hydrogen and allow energy to be stored and transported. Mr Taylor’s support for a national hydrogen industry was met with some backlash however with the Energy Minister stating investment in the technology should be fuel neutral, ie. produced via any means including utilising coal-fired generation to produce the fuel rather than purely utilising renewable sources. The call however was also backed by the need for the hydrogen to have a certificate of origination attached to the sale of the commodity.

In December 2019, it was reported that the Australian Energy Market Operator (AEMO) has procured record volumes of energy reserves for what the Bureau of Meteorology (BoM) is forecasting to be another record Summer in terms of temperatures on the East Coast of Australia. The BoM is forecasting a hot and dry Summer 2020 leading to concerns, particularly for VIC and SA that the two regions could see a repeat of the conditions that inspired both regions in the Summer of 2019 to reach the market price cap after several hours at VoLL (Value of Lost Load) ~ $14,500/MWh ceiling on 24th and 25th of January 2019. The concern that we could see a repeat of these conditions has resulted in AEMO securing 1,600 MW of emergency reserves to assist in keeping the grid energised through summer 2020. The large volume of reserves has not come cheap with an estimated cost of $44 million of which is obviously not guaranteed to be required at all. AEMO has stated that almost 1,000 MW of the reserves secured is available in VIC and SA which have been identified as the “trouble zones” come Summer, with the remaining 600 MW located in NSW/QLD for those extreme conditions days.

The above spot price outcomes resulted in a significant decline in furtures pricing with all curves around the NEM regions and across multiple CAL and Quarterly products all falling away with weaker than anticipated expectations for Summer 2019/2020.

Looking Forward:

Figure 3: Calendar year 2020 forward contracts

$/MWh

NSW

QLD

SA

VIC

TAS

24-Jan-19

$ 70.32

$ 56.36

$ 66.35

$ 71.79

$ 84.96

(as at 31/12/2019)

(Source: ASX)

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Manager Wholesale Clients and Markets, Alex Driscoll on 07 3905 9220.

The World Economic Forum was held late last week in Davos (Switzerland) with foreign leaders all around the globe coming together to talk about the global economy and hopefully generate some fruitful action.

Probably one of the more market shifting proposed schemes put forward at the World Economic Forum was that of European Commission President, Ursula von der Leyen. Von der Leyen’s proposal is a daunting one from Australia’s point of view, as it could have a significant impact on the country’s vast economic dependence on exportation of minerals and goods.

The proposed scheme, labelled the ‘carbon border adjustment mechanism,’ would be a tax applied to carbon-intensive good from those countries that are not pulling their weight as to lowering emissions under the Paris climate accord.

The economy likely to feel the brunt of this proposed tax-scheme would be China, with the scheme’s proposed first target industries being steel, cement and aluminum. Von der Leyen did however message the scheme could expand into the mining and resources sectors.

Although Australia’s most prominent trade partner in the resources sector is China, Europe was a big receiver of coal exports from Australia in 2019 and could very well be in the firing line with constant debate between Australian politicians and other world leaders as to whether Australia is indeed pulling their weight per the Paris agreement.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

Current weather conditions are placing an increased reliance

on the diminishing water catchments across Australia. These water catchments

store water for use by various parts of the local community including drinking

water for residents, irrigation and Electricity generation.

Stanwell recently announced water sustainability is a top

priority for its Tarong Power stations located within the South Burnett region.

Water is an essential necessity for thermal power stations to make electricity. The water is used for steam production and cooling.

Tarong power station consisting of 4 X 350MW thermal units

and a 443MW supercritical unit. These units obtain their water from two

sources, the primary source is Lake Boondooma and secondary from a pipeline

using water from Lake Wivenhoe or recycled water produced under the Western

Corridor Recycled Water Scheme.

Stanwell corporation is focusing on mitigating the impact on

the South Burnett community by reducing the usage of water from Lake Boondooma

to ensure the South Burnett community have access to drinking water. Initial

initiatives used at the power station to reduce the reliance on Lake Boondooma water

include the use of recycled water from the ash dam and stormwater.

Tarong Power Station have access to water from Lake Wivenhoe if Lake Boondooma drops below 34%, currently the Lake Boondooma’s level is 22.95% as of the (Source: SEQWater 2020). Lake Wivenhoe water also comes at an added cost. Water is currently the highest operating cost for Tarong Power Station.

An alternative to using Lake Wivenhoe water is the use of

purified recycled water from the Western Corridor Recycled Water Scheme. The

scheme is not currently in operation, however when operating and supplying

water to Tarong Power Station it will add significantly to the costs of

generation.

Tarong Power Station first used purified recycled water from

the Western Corridor Recycled Water Scheme in June 2008 following a similar

water supply limitation brought on by the 2008 drought.

As a result, the increasing marginal cost to generation

caused by the higher water cost, Tarong Power Station may change its operation

and reduce generation or dispatch its units at higher prices. Under either scenario

this may increase the cost of wholesale energy in Queensland.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The SA Government (South Australian Minister for Energy and Mining) has the power (under South Australian Legislation) to trigger a Retailer Reliability Obligation (RRO) upon informant from AEMO of a one-in-two year peak demand forecast shortfall event as published in the South Australian Gazette 17 December 2019, with the AER confirming and publishing the notice 9 January 2020. For the avoidance of doubt this means that unlike all other regions which require the Electricity Statement of Opportunity (ESOO) to predict an unserved energy event, SA can act independently without approval as such from the AER.

The RRO was trigged for South Australia on the 9 January 2020 for the following periods:

First Quarter (Q1) for Calendar Year 2022

First Quarter (Q1) for Calendar Year 2023.

The periods of concern according to AEMO’s forecasting includes:

each weekday from 10 January 2022 – 18 March 2022 for the trading periods between 3pm and 9pm EST;

**(Peak demand expected to be 3,030 MW)

each weekday from 9 January 2023 – 17 March 2023 for the trading periods between 3pm and 9pm EST

**(Peak demand expected to be 3,046 MW)

A T-3 Instrument has been created and the Market Liquidity Obligation (MLO) of the SA region’s largest generation businesses, Origin, AGL and Engie have been called upon and are to begin trading exchange-listed (ASX approved products) for Q12022 and Q12023 from 7 February 2020.

With the triggering of the RRO, the South Australian Minister has made a T-3 instrument (under NEL Part 7A 19B (1)):

Q1 2022: This T-3 Reliability Instrument applies to the South Australian region of the National Electricity Market for the trading intervals between 3pm and 9pm Eastern Standard Time each weekday during the period 10 January 2022 to 18 March 2022 inclusive. The Australian Energy Market Operator’s one-in-two year peak demand forecast for this period is 3,030 Megawatts.

Q1 2023: This T-3 Reliability Instrument applies to the South Australian region of the National Electricity Market for the trading intervals between 3pm and 9pm Eastern Standard Time each weekday during the period 9 January 2023 to 17 March 2023 inclusive. The Australian Energy Market Operator’s one-in-two year peak demand forecast for this period is 3,046 Megawatts.

With the T-3 instrument created by the SA Energy Minister, this has triggered the MLO, effectively a market making obligation on the parties identified above to reasonably offer liquid exchange-listed products for the identified shortfall periods.

Obligated MLO participants such as Origin, AGL and Engie will from 7 February 2020 begin offering exchanged-listed products for both Q12022 and Q12023.

The triggering of the RRO means retailers and large load consumers can start procuring volume for their forecast demand for Q12022 from as early as 7 February 2020, and no later than 31 December 2020, the T-1 instrument implementation date (13 months prior to the shortfall period identified).

If you would like to know more, please contact Edge on 07 3905 9220.

A new market notice within the National Electricity Market (NEM) posted by the Australian Energy Market Operator (AEMO), one we have not see before was issued to all market participants on the 23/12/19. The market notice requested and served as a reminder for all semi-scheduled and intermittent non-scheduled generators to ensure they update their market availability bids, update their SCADA Local Limit or, if unavailable, advise AEMO control room to implement a quick constraint to the reduced available capacity level; and update intermittent generation availability in the EMMS Portal to reflect reduced plant availability as is required under the National Electricity Rules (NER), per NER 3.7B(b).limits.

This was an interesting constraint for AEMO to issue as it was due to extreme heatwave conditions across the south east coast of Australia, and as with most generating plant, under extreme heat, some form of derating on its physical capacity and output can occur. On the 23/12/19 AEMO’s weather service provider was forecasting extreme high ambient temperatures across all NEM regions, hence AEMO’s market notice to these participants to remind semi-scheduled and intermittent non-scheduled generators to advise AEMO of any reduction in available capacity caused by temperature derating.

Particularly interesting is that the often “set and forget” approach to renewable generators such as solar and wind generators, as classified by AEMO as semi-scheduled generation is being watched with greater scrutiny, particularly after the events of 2016 in SA where a state wide blackout was triggered by a severe weather, damaging more than 20 towers, downing major transmission lines, and with multiple wind farms currently shouldering some of the blame for the state going black due to the wind farms switching off when the transmission lines went down.

Semi-scheduled: A generating system with intermittent output (like a wind or solar farm), and an aggregate nameplate capacity of 30 MW or more is normally classified as a semi-scheduled generator unless AEMO approves its classification as a scheduled generating unit or a non-scheduled generating unit. AEMO can limit a semi-scheduled generator’s output in response to network constraints, but at other times the generator can supply up to its maximum registered capacity (AEMO 2014).

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.

The federal government recently announced an agreement to underwrite new gas turbines in Victoria and Queensland to provide relief from expected high peak prices. The operation of these assets, below the usual short run marginal cost of current open cycle gas turbines (QLD – $106 / MWh – AEMO 2019) will potentially limit the likelihood of high prices or price volatility over the morning and evening peaks resulting in reduced average spot outcomes.

Under the new generation underwriting plan, which was proposed by the ACCC, the government will assure an amount of the electricity generated will be purchased for a set period into the future.

The Victorian generator will be located at Dandenong, south-east from Melbourne’s CBD and the Queensland asset will be located near Gatton, 90km west of Brisbane.

The 132MW Queensland generator is proposed by Quinbrook Infrastructure Partners, while the 220MW Victorian asset is proposed by the APA group.

Mr Taylor (Minister for Energy and Emissions Reduction) has previously said the government had been “hard-nosed” with these projects and each of them would have to prove commercially viable and benefit the jurisdiction in which they were going to operate.

Both projects are expected to commence construction next year once private sector finance has been secured.

If you would like to know more, please contact Edge on 07 3905 9220.