With a career spanning 20 years and experience across many different technologies, Justin brings an incredible depth of knowledge to our development team. He is passionate about accurate reporting and scalable solutions which are the cornerstones of our business. Justin’s experience in the energy industry means he knows what our clients need. By building systems and developing specialised reporting, he gives them time and space to focus on business growth.

What is the best piece of advice you have ever received?

A boss once told me “Assumptions are the mother of all stuff ups.”

Name a place you have never been to and would like to visit. Why?

One of my future goals is to ride a motorcycle from Anchorage Alaska across to Canada and down the entire West Coast of America to San Diego, hopefully with one of my close friends to enjoy the experience.

Who or What inspires you?

One person who comes to mind is Roger Federer. He has been at the top of his game, passionate and above all you never see him disrespect others or complain when he has been beaten when he gave his best.

What is one of the biggest challenges facing energy customers today?

New and exciting technologies can be both a blessing and a curse. Batteries, Solar and Wind are growing in generation every year, however this requires upfront investment in time and money and ensuring the return is worthwhile.

What does a typical day look like for you at Edge?

As an early starter, I get in around 7 am and the first thing I will do is check all our systems for any outages or data files that have not arrived for the day. Then we plan our day and what features we are going to work on that adds value to our customers as well as enhancing any existing systems to make them more robust. Each day throws different challenges and new opportunities which makes my role exciting, which is what I love about working at Edge.

Domestic gas prices on the east coast of Australia have been through a huge transitional period as a result of the introduction of the LNG export market from Curtis Island. Whilst there have been a broad range of changes, one of the key factors increasingly influencing price that domestic consumers pay is the price of oil. Domestic contracts are now being offered at oil linked pricing which effectively means that if the price of oil increases so will the price of your gas (and vice versa). For large gas producers this is nothing new as hedging commodity prices is part of their core business. For consumers however this may be more challenging depending on the products they produce.

Other factors that are now impacting Australian gas prices are:

Climate change policies in Asia as gas is a widely used fuel for clean electricity generation. This is particularly important when considering China due the huge demand and current reliance on coal generation.

Manufacturing levels in Japan

US production levels and construction of pipelines

Renewable energy technology developments

Turning our attention to domestic gas influences the Northern Territory Chief Minister Michael Gunner has recently announced that the 135 recommendations made in the recent inquiry into fracking in the NT would be implemented, allowing on-shore fracking to take place in the territory. The 135 recommendations made in the inquiry mitigate the risks associated with onshore gas development to acceptable levels, and in some cases claim to eliminate the risks completely. New gas developments will require environmental management plans which will be assessed by the NT Environment Protection Authority and signed off by the environment minister. There will also be area’s where fracking will not be allowed. These include indigenous protected areas, special environmental areas, cultural and agricultural areas of significance to the Northern Territory. There is a number of studies to be completed before fracking production can begin including strategic environmental and baseline assessments. At this stage it is estimated that exploration will begin in 2019 and production in 2021.

On 21 May Santos Rejected Harbour Energy’s (Harbour) offer to purchase 100% of shares at US$5.21 per share. In an effort to get the deal over the line Harbour offered $5.25 per share if Santos was willing to extend certain oil price hedging arrangements. The final offer from Harbour had a number of conditions which included Santos assisting with debt raising and hedging a significant portion of Santos oil-linked products as well as FIRB approval. Once the offer was rejected Santos shared its view on how superior shareholder value could be realised through executing the current strategy.

Australian Industrial Energy will see Port Kembla in NSW developed into an LNG import terminal. The Andrew Forest venture recently reached significant milestones. These include receiving backing from Japanese energy giant JERA and signing a memorandum of understanding with 12 potential customers (according the AFR). Project development is still subject to approvals.

AEMO recently released its Victoria Gas planning report update that painted a concerning outlook in respect of depletion of offshore gas fields reserves. The data provided to AEMO from producers in the Gippsland basin forecast production to reduce to 38% below the 2018 production forecast and 68% for Port Campbell. In response to this outlook gas producers and other market participants are investigating additional supply and capacity.

Regional analysis

Narrowing our focus, Edge take a closer look at gas generation in each region and the local gas trading hub. As we know the Federal Government threatened LNG producers with the Australian Domestic Gas Mechanism late last year if they didn’t allocate more gas to domestic consumers. The threat appeared to have worked with each of the LNG producers advocating that they had made gas available.

When we take a closer look at whether a relationship exists between gas generation and gas hub prices we realise that it is difficult to discern. Limitations in access to pipeline capacity, contractual arrangements and sophistication of users are potentially key drivers behind this.

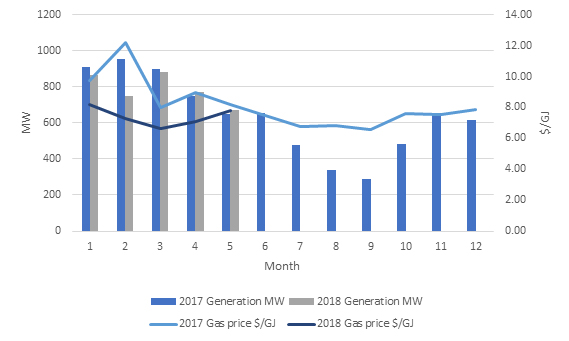

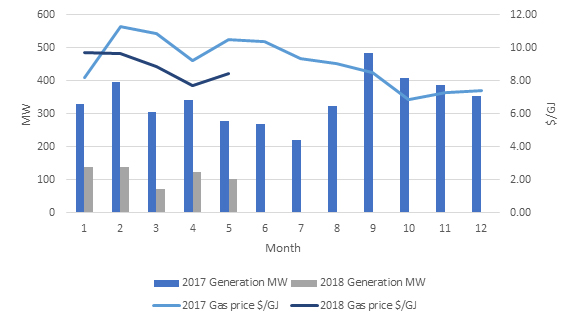

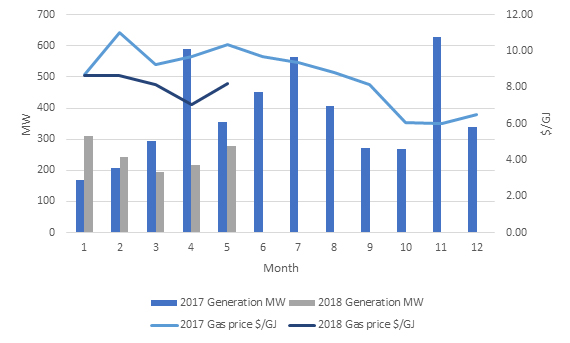

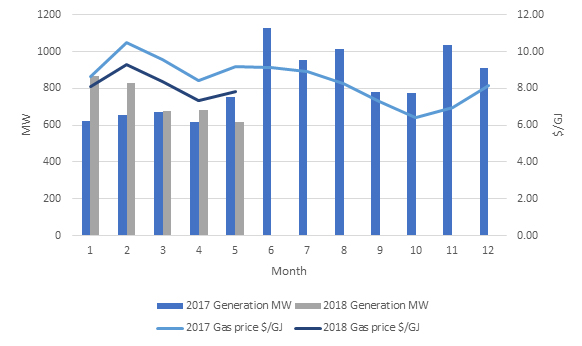

The following graphs display average gas generation from 1 January 2017 to the end of May 2018 on a regional basis as well as the average gas price for the same period.

Queensland

From the graph we can observe that gas generation in 2018 (to date) is largely in-line with 2017. The consistent level of generation is interesting given the significant decline in spot electricity prices in Q118 relative to that of Q117. On face value the lower spot prices in 2018 would result in less generation from gas power stations. What changed however between Q117 and Q118 was SwanBank E power station returned. The gas combined cycle power station ran consistently throughout Q118 averaging 237 MW of generation. Lower spot prices in the Brisbane STTM are a driven by lower demand and potentially increased supply as a result of the LNG producing increasing availability of gas to domestic consumers.

New South Wales

NSW gas generation was significantly down for the first 5 months of 2018 relative to the same period in 2017. Lower gas generation in NSW was largely the result of less volatility in the electricity spot market. If we look at the bid stacks of the large gas power stations in NSW, Tallawarra was the most motivated to produce energy offering up to 210 MW at below zero dollars. This strategy could not be observed at Uranquinty or Colongra.

Victoria

Unlike NSW and QLD generation from gas powered power stations increased in January and February 2018 relative to the same months in 2017. The closure of Hazelwood power station in late March 2017 meant that the 1,225 MW (average generation of Hazelwood in Q117) was no longer available. Less baseload generation in the region resulted in higher electricity prices which meant that gas power stations were dispatched more regularly. Despite the increases in generation there was a decline in VIC gas market prices.

South Australia

Gas generation in SA has been heavily impacted by the increased level of intervention in the SA market by the market operator. The market operator has been constraining off wind generation and calling on gas generation which has increased overall generation from gas plant. This increased generation however has not translated into higher gas prices as we can see from the graph these 2018 prices are trending below 2017 prices.

When observing each of the regions and the time periods selected it is fair to say that generation from gas fired power stations and spot prices in the gas hubs do not drive average price outcomes.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220 or contact your Edge Portfolio Manager.

By Thomas Dargue, Edge Manager of Markets & Advisory

The electricity market was active throughout autumn and the transition into winter. Spot prices were largely stable as has been the case ever since the Queensland Government directed Stanwell Corporation to adopt strategies to lower wholesale prices and Snowy Hydro Corporation seem to be willing to draw down their dam levels to keep prices in New South Wales below $300.00/MWh for each trading period.

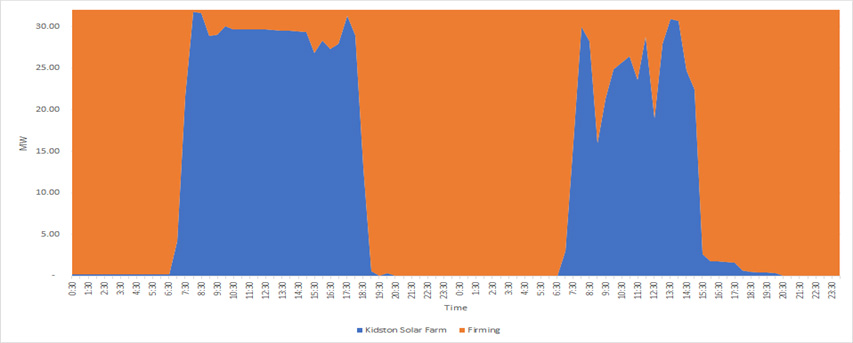

Stable spot prices doesn’t mean that the market has been uneventful. In Queensland utility scale solar is expected to grow from only having Barcaldine Solar Farm (25 MW capacity) to more than 2,000 MW installed by the end of 2019. In November 2017 Kidston Solar Farm (50 MW capacity) started generating and since April 2018 we have seen the addition of Sun Metals, Clare, and Longreach solar farms with a combined capacity of 248 MW. Other solar farms are being commissioned at the moment including Hamilton, Whitsunday and Hughenden which means that Queensland will soon have 453 MW of utility scale solar. This is in addition to the small scale solar installed already in Queensland which is more than 2,000 MW and continuing to grow.

New South Wales continue to struggle with sufficient capacity.

To date Snowy Hydro has increased its output when prices looked like it was going to go above $300.00/MWh. This strategy has appeared to be successful with only two prices above this level ($300.80/MWh and $301.06/MWh on 25 July 2017 at 18:00 and 18:30 respectively) since the start of 2017. This defence of prices has come at a large cost to the dam levels with the main dam, Lake Eucumbene, dropping below 30% full which is the lowest level since 2011. In early June 2018, constraints prevented much of Snowy Hydro’s portfolio from being dispatched and the New South Wales prices spiked to $2,428.77/MWh and $2,447.89/MWh on 5 June at 17:30 and 18:30 respectively. The high prices followed large cloud cover reducing generation from solar farms and the removal of several large coal plant due to planned or unplanned outages. These outages persisted and there was another price spike on 7 June 2018 at 19:00 where prices in New South Wales reached $2,464.52/MWh. On both days where the prices were high, AEMO had warned that there were insufficient reserve of generation and Tomago Smelter had demand curtailed under their agreement with AGL.

Victoria was comparatively quiet during autumn. Spot prices remain high in a historical context with the period from 1 April to 30 June averaging $94.92/MWh – more than $10.00/MWh higher than New South Wales over the same period.

Victoria use to enjoy an abundance of cheap generation from their brown coal generators however have seen more imports from South Australia and New South Wales since the closure of Hazelwood Power Station. Victoria has an old fleet of highly polluting power stations and need an orderly transition to avoid suffering intermittent issues seen in South Australia.

Tasmania continues to manage their dam levels to avoid the constraints on local manufacturing plant which was experienced during the last extended outage on Basslink. There was trouble on the interconnector again with no flow between 24 March 2018 and 5 June 2018 following an accident during maintenance. The highly specialised nature of the underseas cable means that parts take a long time to procure and then be installed. Overall the state managed to supply electricity throughout the period. The reliability of Basslink is a further cause for concern as Tasmania is trying to become the “battery of the nation” by using its abundant pumped storage hydro sites to effectively store energy while there is excess renewable generation and produce electricity when there is less renewable generation being produced. If the electricity cannot be reliably transferred in and out of Tasmania, the investment decision is less attractive.

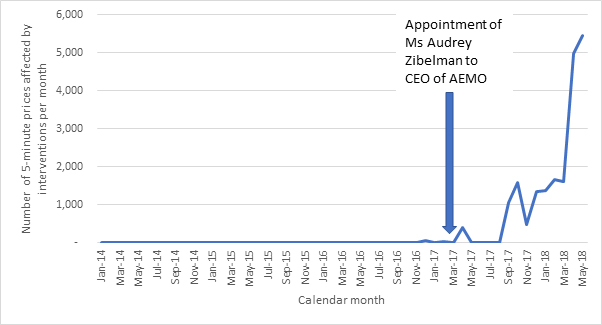

South Australia had more price periods affected by market intervention during May 2018 than any other time in the past. More than half (61%) of the time, the prices were affected by directions from AEMO.

Some of this is due to Pelican Point coming off 23 April 2018 and not returning until 23 May 2018. An intervention price occurs when AEMO has directed a participant (typically a generator) to dispatch in a different way to its bidding. This was typically used to direct a gas or diesel power station to operate through periods where the owner expected it to not be commercially viable to operate. This was done to strengthen the grid by securing sufficient synchronous generation remains online at all times. AEMO then calculates how the market would have settled if they hadn’t issued the direction. This calculation doesn’t take into account the fact that bidding may have been different if the direction hadn’t been issued. Participants could have chosen to turn on voluntarily or wait for higher prices. As such, this will distort the pricing signal provided in the market. Even though spot prices tend to be lower during these directions, participants that are directed are entitled to compensation which is ultimately paid for by the consumers. When the price signal is taken out of the spot market and put directly onto retailers (who pass the costs on), there is little incentive to solve the issue. The total amount of interventions have increased dramatically as the system is getting weaker however it also seems to be part of a new direction from AEMO. To put the number of interventions into context, there were roughly 20 times more intervention periods in May 2018 (5,451) than the 10 years prior (228) to the appointment of the CEO Audrey Zibelman.

Figure 1: Number of prices affected by intervention from AEMO

If the intervention continues, the spot prices will remain lower however the cost to the consumers could increase.

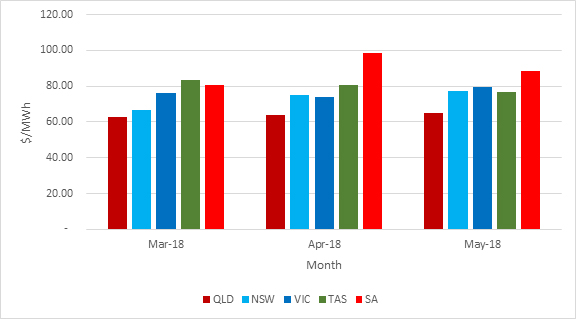

Overall spot prices were lower than the summer period with the cheapest spot prices being in the North and the East. Queensland had the cheapest prices followed by New South Wales and Victoria. Tasmania managed to end the period with lower prices than South Australia despite Basslink being cut off for part of the period.

Figure 2: Average monthly spot prices in the NEM

The more stable spot conditions saw the forward prices decrease across all the traded regions. The largest fall was in Victoria where prices reduced $8.97/MWh for calendar year 2019 contracts. New South Wales also reduced $8.43/MWh as spot prices remained stable. The forward prices are now similar across Victoria, New South Wales and Queensland however South Australia continues to trade higher than the other regions. This is in part due to expectations that the spot prices are likely to stay higher than elsewhere and partly as firm contracts are more difficult to get as many renewable generators are unable to offer firm prices. Recently Snowy Hydro has been acquiring power purchase agreements with renewable generators and released a tender for up to 800 MW of additional renewable generation. It is likely that Snowy Hydro will use its pump storage hydro plant to firm up the renewable generation offering more firm contracts.

Table 1: Calendar year 2019 forward contracts

NSW

QLD

SA

VIC

1 March 2018

76.58

64.05

94.36

82.9

31 May 2018

68.15

62.64

87.00

73.93

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Manager of Markets & Advisory, Thomas Dargue on 07 3905 9226 or on 1800 EDGE ENERGY.

Oliver is one of our staff members Justin’s’ eldest 10-year-old son. A couple of years ago he was diagnosed with Autism Spectrum Disorder (ASD). He is a very smart, intelligent and loving boy and is known as a High Functioning Autistic, which you may have heard of in the past called Asperger’s syndrome.

Autism affects roughly 1 in 59 children and 1 in 37 boys. Children like Oliver find it hard to fit into the standard schooling system often requiring extra resources that are not always available. Luckily for Oliver, he has recently been accepted to attend the Autism Queensland School on a part time basis. Oliver will split half his time between his regular school and Autism Queensland School to give him all the tools in life outside of pure academics. Each class only has 6 children in it of a similar age and skill set to allow for a more tailored and effective educational experience. Edge would like to wish Oliver and his family all the best for his first day at Autism Queensland School.

Children like Oliver benefit from these services due to generous donations by the public. You too can assist in making a difference in these children’s lives by donating here https://autismqld.com.au/page/make-a-donation.

Edge focuses on ensuring the information we hold about your business’s energy costs and consumption is safe and secure. We also like to ensure that information is only provided to parties within your business, that are authorised to have access to that information. A challenge for Edge has been to maintain this security requirement through the use of Edge Live, whilst also ensuring it widely accessible by staff within your organisation as possible.

We have recently added some features to Edge Live that can provide you comfort when it comes to providing the right people with access to the right information within your organisation.

As an Edge Customer, you are provided your own unique ‘tenant’ within the Edge Live system. Some of our larger customers have multiple tenants, reflecting the organisation of their various business units. Each user is assigned access to one or more tenants. Data is held securely within the scope of a tenant and cannot be viewed unless a user has access to that tenant.

We have recently extended Edge Live to support a hierarchy of tenants. A particular tenant may have a parent tenant, or multiple child tenants. This hierarchy can be set up in Edge Live to reflect the organisation of your business. This means that a user can easily view data across multiple areas of your business, without having to switch between tenants.

Edge Live data (e.g. sites, invoices, reports, and contracts) is associated to particular groups. A tenant can have multiple groups. While users generally have access to all groups within a tenant, they can be restricted to only view the data belonging to one or more groups.

Not only do these features ensure the security of your information, it also helps us to effectively communicate only relevant data and information with members within your organisation. For example, on-site personnel may be restricted to reports, meter data, or dashboards associated with the particular site at which they work. Finance personnel may only have access to accrual and invoice reconciliation dashboards and your invoices.

By defining the type of information your staff can access via Edge Live, we can be confident that the information that we provide is relevant to the role they perform, thus giving them the information they need to make informed decisions.

Speak to your Portfolio Manager today about how we can configure your Edge Live tenant and its groups to maximise Edge Live’s userability within your organisation.

The Energy Security Board (ESB) released a new version of the proposed National Energy Guarantee (NEG) following feedback from a variety of interested parties. The ‘Draft Detailed Design of the National Energy Gurantee: Consultation Paper’was released 15 June 2018. Also included was a paper by the Federal Government setting out the proposal for key areas of legislation which will be set at a Federal level. To support the papers a number of technical working papers were released to explore key aspects of the NEG.

The new version remains focused on reducing emissions in line with Australia’s commitment under the Paris Agreement and ensuring reliability. In addition to these key priorities, a third priority was to ensure that electricity remained affordable going into the future.

In regard to emissions, the largest change from the original version is a voluntary decoupling of the electricity contract written and the emissions levels. A retailer will still need to purchase contracts to keep emissions below a set threshold, however the emissions will no longer have to come from the same contracts that they have purchased electricity from. In theory, a retailer can purchase the output of a coal fired power station however not take on the emissions. That retailer would then be exposed to the emissions at the spot market which could be met through a separate contract with a renewable generator for only the emissions component.

In practical terms, the current proposed NEG is for all intents and purposes a cap-and-trade scheme. A retailer will be provided a cap on emissions. If they exceed that cap, they will have to purchase emissions credits from a low emitting source. If they are under the cap, they can sell their over commitment to other retailers. There will be the option to carry forward a limited amount of a previous compliance year’s over-achievement, for use in a later compliance year.

Reliability will come from AEMO’s forecast of supply adequacy. Each year, AEMO estimates supply adequacy for the following 10 years. If a material gap is identified, AEMO will notify liable entities (likely to be retailers and large users 5MW or greater) that there may be a reliability obligation. If the material gap is still present 1 year out, AEMO may start procuring demand response or additional generation. At this stage all liable entities must disclose their contract position to the AER. If a period with a projected reserve gap has demand above a one-in-two-year event, AER will monitor compliance against the reliability target. Each liable entity must demonstrate that they have procured sufficient qualifying contracts (such as fixed price contracts of a suitable nature, demand side management, or firm generation) to cover their position during peak demand. It is proposed that a reliability gap will also trigger liquidity obligations for vertically integrated retailers to make financial contracts available to the market via the central exchange. Furthermore, it is proposed that large users may transfer their reliability obligation to their retailer, but will have to ensure that their Electricity Sale Agreement addresses this. If a liable entity has insufficient qualifying contracts, penalties may apply. The level of penalties is undecided however a suggestion has been made to link to AEMO’s cost of procuring responses.

As with anything, the cost of both the emissions and the reliability components

of the NEG is likely to be passed on to consumers.

Modelling done to justify the introduction of the NEG assumes that the certainty brought by the NEG will reduce the risk premium of new power stations and cause more trading to occur. Both these factors would likely bring down energy prices (compared to business as usual). However, if the market does not see this as a much more stable investment environment, a reduction in wholesale prices is unlikely to materialise.

The NEG will expose consumers to both emissions and reliability costs. In terms of the emissions component, for most consumers this will be another pass-through cost added to their bills. Any trigger of a reliability gap could drive the cost of acquiring qualifying contracts (such as financial contracts) much higher in the relevant period. Whilst the liquidity obligation aims to counter this, we have concerns around how this will be enforced. It is critical to protecting against extortionate costs under this component. The current version of the NEG discusses a number of ways of addressing this and the ESB recommends creating a new repository for contracts as well as a market liquidity obligation. The repository would be able to report on all over-the-counter (non-exchange traded) products including volume and price. This may only be reported in aggregate for the market instead of identifying the parties to the deal. Very little detail is provided regarding the register. The market liquidity obligation would require large vertically integrated retailers to make contracts available where there is a reliability gap. The retailers must offer to buy and sell contracts at a maximum spread so that prices can’t be set too high for buyers and too low for sellers. As with the repository there are few actual details on the liquidity obligation.

The emissions component has the potential to be highly variable from retailer to retailer. Each retailer will look at the generation they have produced and what emissions contracts they have purchased. If they haven’t purchased sufficient contracts for their entire load, they will assume to have procured the rest at spot. The spot emissions is calculated as the total emissions intensity of all generation less the generation volume already contracted in the emissions registry. A retailer or consumer is unlikely to know in advance how much will be forward sold and therefore the emissions costs can be highly uncertain. The retailer is likely to pass through this cost directly to the consumers, who ultimately wears the risk.

It is critical for all consumers who are agreeing electricity contracts with their retailers to understand how things such as the NEG are managed by their retailer and passed through. For the more sophisticated purchasers there is an opportunity to proactively manage some of this exposure themselves.

The Federal Government will continue to make laws regarding three key areas of the NEG. The key areas are:

Setting emissions targets

Treatment of emissions-intensive trade-exposed industries; and

The role of external offsets

There is a separate paper exploring these issues. The emissions targets are proposed to be expressed in tonnes of CO2-e/MWh. The target will be to meet a 26% reduction on 2005 levels by 2030. This is the target which was set at the Paris Agreement. There has been some criticism that if electricity only meets their proportion of the reduction, all industries will have to make the same reductions. The criticism is that it is much more economical to meet a greater share of the obligation from the electricity sector where alternatives to carbon emissions are cheaper than in other sectors.

The Federal Government is proposing to keep emissions-intensive trade-exposed industries exempt from the NEG obligations. This is to maintain international competitiveness.

This means that the rest of the electricity market will be required to purchase

additional volume to make up for the exemptions.

The paper also discusses the role of external offsets including the Australian Carbon Credit Units (ACCU) which are currently part of the Federal Government’s safeguard mechanism. They have also opened up to the possibility of allowing a limited number of overseas certificates be used for surrender.

There are still some large outstanding issues with both the ESB and the Federal Government’s papers. The ESB is pushing ahead to get a decision from the COAG Energy Council in August 2018. To facilitate this date, the turn-around time for comments are limited. The Federal Government is seeking comments by Friday 6 July 2018 and the ESB wants their comments by 13 July 2018. The commencement date of the NEG is due to be 1 July 2020.

If you would like to understand more about the NEG and the potential impact it may have on your energy portfolio moving forward, please visit edge2020.com.au or alternatively you can call one of our team directly on 07 3905 9220 or on 1800 EDGE ENERGY.

Edge attended the Gas Energy Australia 2018 National Forum held at the Gold Coast on 17 and 18 May 2018.

There were a number of prominent speakers at the forum including Senator Canavan, the Commonwealth Minister for Resources and Northern Australia; Tony Wood, Energy Policy Director at the Grattan Institute as well as Ian Macfarlane from the Queensland Resources Council.

Senator Canavan highlighted the improvement in the gas prices during the first four months of 2018 compared to the same period in 2017. He attributed part of the 24% reduction in prices at the Wallumbilla gas hub to the conversations the Federal Government had with key gas producers last year and the potential for a domestic reserve policy being enacted. The Senator also highlighted some of the challenges in communicating the value of having gas being produced right across Australia. He noted that it costs around $2.00/GJ to transport gas from Queensland to Victoria and only between $2.50/GJ and $3.00/GJ to transport gas from Queensland to Japan. The Senator had praise for the Northern Territory Government for allowing more exploration. The is a potential for 1 billion barrels of oil to be extracted in the Northern Territory which would alleviate some of the energy security issues that Australia is facing.

The Senator also spoke about some of the issues in the electricity market. He confirmed that the current renewable energy target would be closed off to new participants starting after 1 January 2021. He described the renewable energy target as one of the worse policies ever.

Tony Wood of the Grattan Institute agreed that the cost of the renewable energy target did not justify the carbon reduction. He also reflected that energy policy would continue to be political and it was up to industry to drive it forward.

Ian Macfarlane agreed with previous speakers on the renewable energy target. He described having to implement the original scheme as a “hospital pass” handed down from previous ministers. He also went on to talk about the importance of the gas industry and how the industry needs to be better at engaging the wider population. He mentioned the importance of countering the rhetoric from activists trying to stop the industry growing particularly on social media where the gas industry historically was underperforming.

If you would like to know more about the outcomes of the forum, please contact Edge on 07 3905 9220 or 1800 334 336.

Edge presented at the Gas Energy Australia 2018 National Forum which was held on the Gold Coast on 17 and 18 May 2018. The presentation was aimed at showing the opportunities the changes in the current electricity market held for gas producers. As the electricity market continues to adopt more renewable energy, there is an opportunity to firm this energy by supplying power when the relevant renewable source is not operating.

With an increasing demand for firmed renewable products this is a perfect time for gas producers to consider power generation in support of the renewable industry. It is possible to partner up and deliver the types of products that consumers want, and retailers are able to pass through.

If you would like to know more please contact Edge on 07 3905 9220 or 1800 334 336.

Edge has been invited to present at the Gas Energy Australia 2018 National Forum, which is being held over the next two days on the Gold Coast. The forum seeks to provide important insights and new learnings across a range of industry relevant issues including policy, innovation, supply and security of Gas within Australia.

Gas Energy Australia is the national peak body which represents the bulk of the downstream gaseous fuels industry which covers Liquefied Petroleum Gas (LPG), Liquefied Natural Gas (LNG) and Compressed Natural Gas (CNG). The industry comprises major companies and small to medium businesses in the gaseous fuels supply chain – refiners and supplies, fuel marketers, vehicle and equipment manufacturers, vehicle converters, consultants and other providers of services to the industry.

Thomas Dargue, our Manager of Markets and Advisory, will be presenting on innovative distributed energy solutions and gaseous fuels highlighting some of the opportunities that the change in the National Electricity Market could bring to gas producers.

If you would like to know more about Australian gas or discuss what changes are on the horizon in the gas market both short and longer term, please contact Edge on 07 3905 9220 or 1800 334 336.

With a career spanning 20 years and experience across many different technologies, Justin brings an incredible depth of knowledge to our development team. He is passionate about accurate reporting and scalable solutions which are the cornerstones of our business. Justin’s experience in the energy industry means he knows what our clients need. By building systems and developing specialised reporting, he gives them time and space to focus on business growth.

With a career spanning 20 years and experience across many different technologies, Justin brings an incredible depth of knowledge to our development team. He is passionate about accurate reporting and scalable solutions which are the cornerstones of our business. Justin’s experience in the energy industry means he knows what our clients need. By building systems and developing specialised reporting, he gives them time and space to focus on business growth.