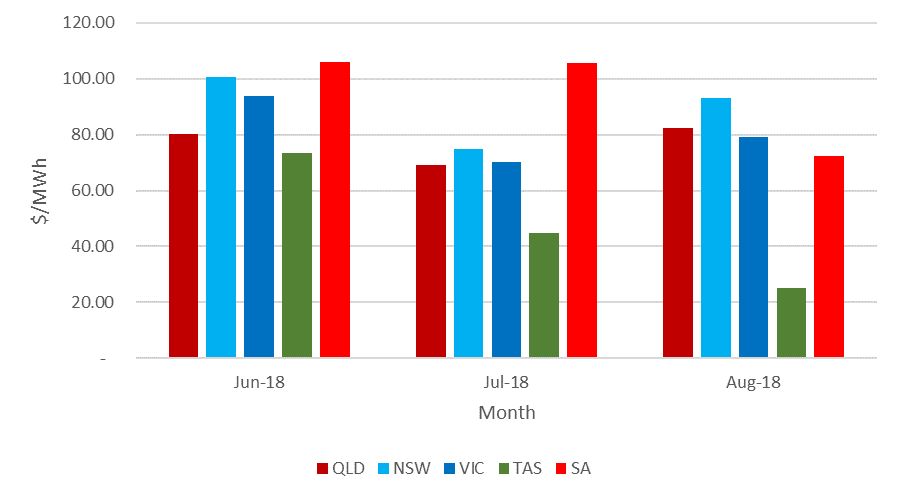

The electricity spot prices were generally higher for the winter period (June to August) than the preceding three months. The largest contributing factors were higher gas prices and increased demand for most of the regions. This excludes Tasmania where average prices fell from $80.26/MWh in autumn to $47.55/MWh in winter. Demand was still higher in the Tasmanian region, however additional rain meant that many of the hydro plants were running, as opposed to spilling water without generating. This put downwards pressure on the local prices.

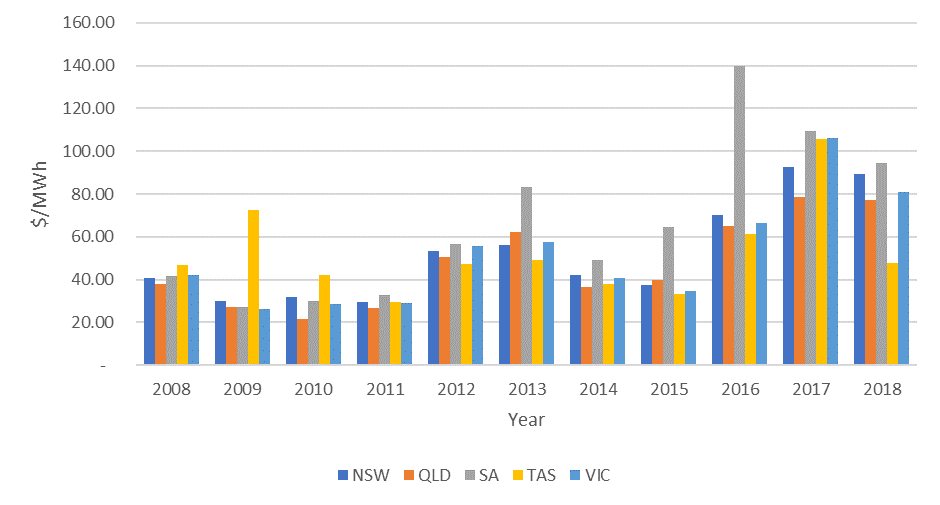

The lower Tasmanian prices didn’t result in lower prices for the rest of the National Electricity Market (NEM). Across all regions, the prices during the 2018 winter were lower than the 2017 winter, however were still very high in a historical context. Looking back across the last 10 winters, the previous two (three for South Australia where Northern Power Station closed in May 2016) look like outliers. In fact, averaging the previous 8 years from 2008 to 2016, prices have been lower for all regions.

Figure 1: Historical prices for winter

It should be noted that prices in both 2012 and 2013 were affected by a carbon tax, which was subsequently repealed in 2014. Since then, there has been a steady price increase in all mainland NEM regions. The prices appear to have plateaued, however not reduced. In Queensland, the Government provided a direction to Stanwell Corporation to adopt strategies to reduce wholesale prices. Since the direction, there have been fewer price spikes (prices above $300/MWh). Although, the prices outside summer months are not reducing. Queensland is the only NEM region which had lower demand during winter compared to autumn. Price spikes in June caused by issues on the transmission network and lower availability at the start of winter kept average prices higher.

New South Wales had the same transmission issues as Queensland, and rolling planned outages at coal fired power stations meant that there was little spare base load capacity available. Victoria had high overall prices with few price spikes and was the only NEM region which didn’t have any prices above $350/MWh. Higher demand and gas prices kept overall prices high in the region. With lower availability in New South Wales, Victoria exported an average of 389 MW into the region compared to 57 MW during autumn. South Australia is heavily dependent on gas powered generation when there is insufficient renewable generation to power the state. This makes South Australia vulnerable to higher demand and higher gas prices, both of which were prevalent during winter. Prices were the lowest in three years, however still the highest of any NEM region. There is still a large amount of domestic gas usage in South Australia which means that prices tend to spike during winter. This occurred again in 2018.

For a full report on our gas prices see here.

Figure 2: Average monthly spot prices in the NEM

The market didn’t run completely smoothly during the winter period. On Saturday 25 August 2018, multiple simultaneous lightning strikes on critical infrastructure caused load shedding. The lightning strikes occurred on the border between New South Wales and Queensland causing a loss of the main interconnector between these two regions. At the time, Queensland was supplying New South Wales with generation. The sudden loss of generation from Queensland caused load to be tripped in New South Wales. The loss of frequency also triggered a shutdown of the interconnection between South Australia and Victoria for reasons still being investigated by AEMO. This caused load shedding in Victoria and Tasmania. In total, 800 MW of load was lost in New South Wales, 280 MW in Victoria and 80 MW in Tasmania. This was predominantly industrial load which was reconnected within an hour.

Higher spot prices and concerns over the stability of the grid has caused the forward prices to increase. Snowy Hydro continued to draw down on its dam levels and with a dry outlook, the inflows could be lower than previous years. If Snowy Hydro reduces their output during 2019, spot prices could be even higher than current prices.

We are also seeing a separation between prices again. Though there were increases across all states, these were highest in Victoria ($16.56/MWh) and New South Wales ($15.88/MWh), and lowest in Queensland ($7.38/MWh).

Figure 3: Calendar year 2019 forward contracts

| NSW | QLD | SA | VIC | |

| 01-Jun-18 | 68.18 | 62.53 | 87.00 | 74.00 |

| 31-Aug-18 | 84.06 | 69.91 | 96.09 | 90.56 |

Source: ASX

There continues to be additional generation added to the market, mainly renewable energy. Going forward, it will be the integration of this renewable energy into the market which will ultimately determine if prices will reduce or if a more volatile market will be created. It is certainly unlikely in the near term that spot prices will return to historical levels (where the cost of energy during winter was in the $30s/MWh).

Looking forward

Q119 continues to be a period of concern across the market, as market participants continue to accept higher prices for swaps in the interest of reducing or removing exposure to spot prices. The BOM is forecasting hot and dry temperatures during the period, which are conditions that tend to cause volatile and higher spot prices.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Energy Analyst, Nick Clark on 07 3905 9227 or on 1800 EDGE ENERGY.