The electricity market is in a state of confusion as a result of poor Federal and State Government policy. The Market Operator, AEMO, released the Electricity Statement of Opportunities during September. The Statement warned of supply shortfalls during the first three months of 2018 and a heightened risk of unserved energy over the next 10 years.

On 17 October the Federal Government announced the National Energy Guarantee (NEG). The Guarantee is the model that will see energy being delivered to consumers reliably and affordably whilst also meeting our international emission commitments. The NEG is an alternative to the Clean Energy Target introduced by Dr Alan Finkel in his Finkel Review. Since the announcement of the NEG, there has been minimal feedback by the Federal Opposition and some of the State Governments. These governments have made it clear they are waiting on further detail before giving their support. Without support from these governments it will be difficult for the NEG to get off the ground. Edge are awaiting further announcements and modelling from the Federal Government as there is insufficient detail to form a view on the impacts or functionality of the Guarantee for producers and consumers of energy.

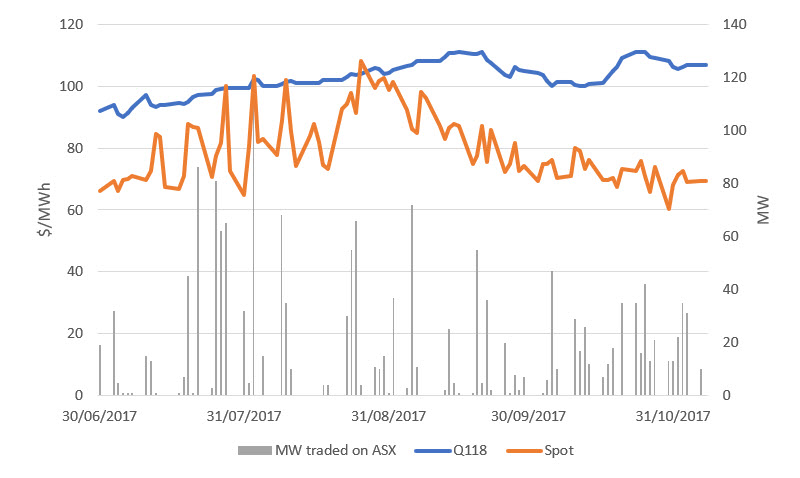

The combination of forecast shortfalls in energy supply, and a national energy policy that lacks detail, has resulted in the price of forward contracts creeping up despite softening spot prices. This has been particularly evident in NSW.

Figure 1 NSW daily average spot price verse CAL18 price and volume traded on the ASX.

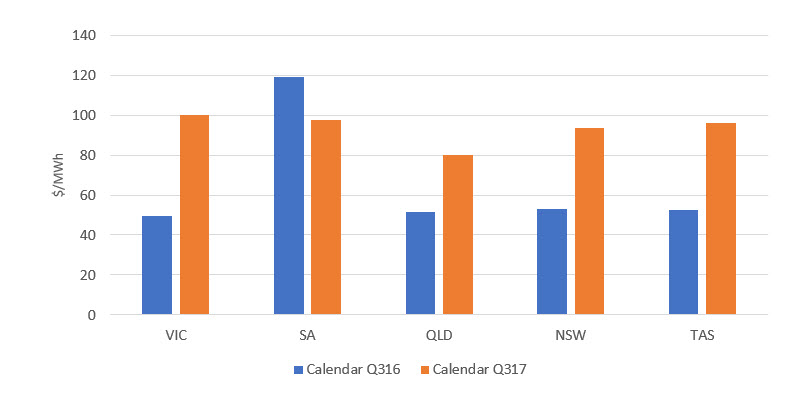

With the exception of SA, average spot prices for Q317 are significantly higher than Q316 prices. This represents a fundamental shift in the market.

|

VIC |

SA | QLD | NSW | TAS | |

| Calendar Q317 | 100.01 | 97.74 | 79.93 | 93.57 |

95.84 |

Table 1 Q317 average spot prices as at 7 November 2017.

Figure 2 Q316 verse Q317 average spot prices.

With valid concern around shortages in supply, medium to large energy consumers are looking for alternatives to reduce costs and/or hedge price risks. A credible alternative is a Power Purchase Agreement (PPA); entered into directly with a generator. PPAs can be facilitated with any kind of generator that is willing to offer one. Typically, these are renewable energy projects offering 10 – 20 year agreements at defined prices. This type of offtake agreement is generally required prior to a new renewable project receiving financing. Offtake agreements from renewable projects do not suit all customers and the following points are some key considerations that should be taken into account before entering a PPA with a renewable generator:

- Ability to commit to a volume and price for 10 or more years

- Correlation of your demand and the output profile of the renewable generator

- Business view on hedging commodities

Click here if you would like to read more about how Edge is assisting customers to reduce costs through the implementation of PPA’s.

Supply Near Term outlook

Spot prices are expected to be volatile and high due to a shortage in supply. Particularly in the first three calendar months of 2018 in SA and VIC. This expectation is a driver behind the Reliability and Emergency Reserve Trader (RERT) and a reason for forward contracts being traded at high prices.

| VIC | SA | QLD | NSW | |

| Q118 | 146.00 | 159.00 | 105.35 |

106.76 |

Table 2 Q118 Forward Contract Prices as at 7 November 2017.

The second round of the Long Notice RERT was released on 6 September 2017. The purpose of the RERT is to provide AEMO with the capability to maintain power system reliability and system security by utilising reserve contracts. In order to become a member of the RERT Panel, panellists need to either provide generation or load reduction.

Submissions were due on 20 September and contracts are required to be executed by the 31 October 2017. Currently, there is a Medium to Short Term RERT open to tender which is scheduled to close on 17 November. Participants are asked in this tender what their reserve availability will be in the period 1 November 2017 to 31 March 2018.

The recent commitment from LNG producers to make more gas available to the domestic market should alleviate some of the predicted high electricity prices. It has to be noted however, that this additional gas is in QLD which is a long way from SA and VIC where the main concerns sit. This gas is more likely to relieve prices in QLD which in turn should help to mitigate high spot prices in NSW, though impacts will be marginal further south.