The Queensland State Government increased the petroleum royalty rate by 2.5% to 12.5% in the 2019/2020 budget, claiming that it will increase revenue by $467 million over the four years ending 2022/2023. The increase received condemnation from LNG producers and their investors. In the announcement, Queensland Treasury drew comparison to royalties in the USA and Canada. The resources sector at large has claimed that the higher tariffs put future investment and jobs at risk.

AGL announced during the week that it anticipates first gas to be delivered from its proposed LNG import terminal in the second half of FY22. Originally, AGL indicated that gas would be delivered during FY21, however it is understood that environmental requirements as set by the Victorian Government have caused delays. AGL announced that the floating storage vessel, Hoegh Esperanza would be utilised for the job. It is estimated that the LNG import terminal will be able to send between 80-100TJ/gas per day.

Hydrogen

The COAG Energy Council Hydrogen Working Group has released 9 issues papers which are to help develop the National Hydrogen Strategy. The nine papers released are:

- Hydrogen at scale

- Attracting hydrogen investment

- Developing a hydrogen export industry

- Guarantees of origin

- Understanding community concerns for safety and the environment

- Hydrogen in the gas network

- Hydrogen to support the electricity systems

- Hydrogen for transport

- Hydrogen for industrial users

The hydrogen strategy revolves around producing hydrogen from renewable energy sources to create “clean” hydrogen. Australia has recognised its competitive advantage in producing clean hydrogen due to the solar and wind (renewable electricity required in production of clean hydrogen) resources. The market for hydrogen is currently small relative to other energy sources such as gas and coal however with increasing appetite for low emissions fuel it is anticipated that this will grow. The potential size of the market is unknown. Unsurprisingly parties that stand to benefit from hydrogen becoming a more widely used fuel source anticipate huge growth whereas the more moderate are generally in a wait and see phase.

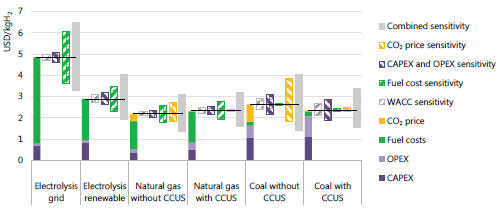

Currently cost of producing hydrogen remains high and makes the fuel uncompetitive as well as having no commercial scale shipping capacity. Hydrogen production costs for different technology options according to the International Energy Agency are summarised below:

Source: International Energy Agency. “The Future of Hydrogen, seizing today’s opportunities” June 2019 p.g. 52

It cannot be understated how substantial the task is to deliver on the COAG Energy Councils vision of Australia becoming a major clean hydrogen player. The table below provides a high-level timetable for actions to 2030 as prescribed by the COAG Energy Council.

Gas Powered Generation

Gas powered electricity generation has been, is, and will continue to be critical to ensuring reliable electricity supply in the NEM. Recently, gas has started to become displaced by new renewable generation in the NEM. Gas however remains critical at times of tight supply and demand balance. The graph below summarises the daily gas used for gas powered generation (Source Australian Energy Regulator) dating back to Q308.

Source: AER

On aggregate we can see that gas generation reached its minimum level since Q308 in Q418. This is primarily driven by new renewable generation in the form of wind and solar. Queensland gas demand has declined after Q414 on the back of Swanbank E mothballing. We also note the rise in SA which corresponds with the closure of Northern coal power station in SA. As the energy market continues to transition to intermittent renewable fuel sources and a 5-minute market, there is interest in adapting existing gas power stations to be able to respond more quickly.

Regional analysis

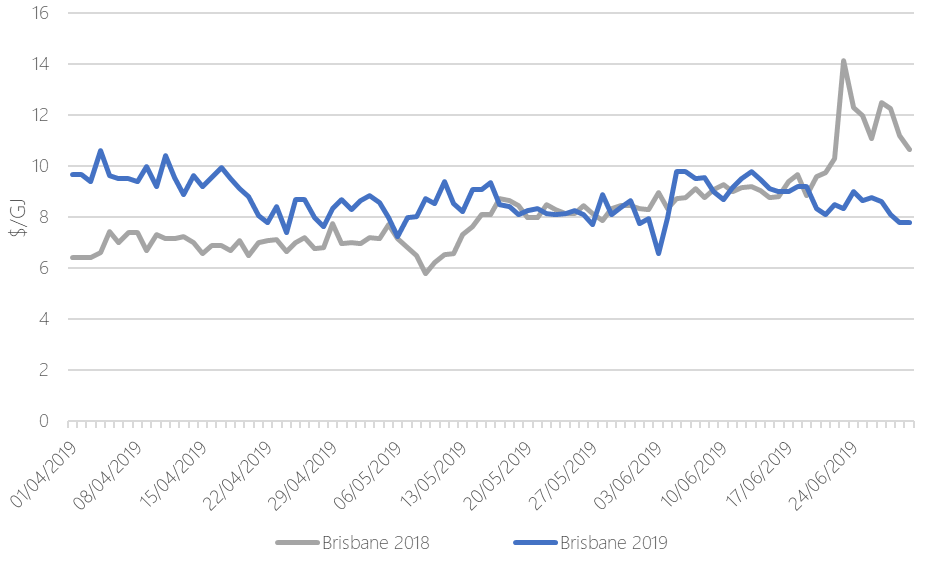

Brisbane

Gas prices in the Brisbane STTM were marginally higher in Q219 relative to Q218, averaging $8.72/GJ. There was no material change in volumes traded through the STTM.

(Source: AEMO)

Sydney

Sydney Q219 average STTM price was $9.79/GJ, which was $1.26/GJ higher than the Q218 average price. Prices during Q219 were highest at the beginning of the month.

(Source: AEMO)

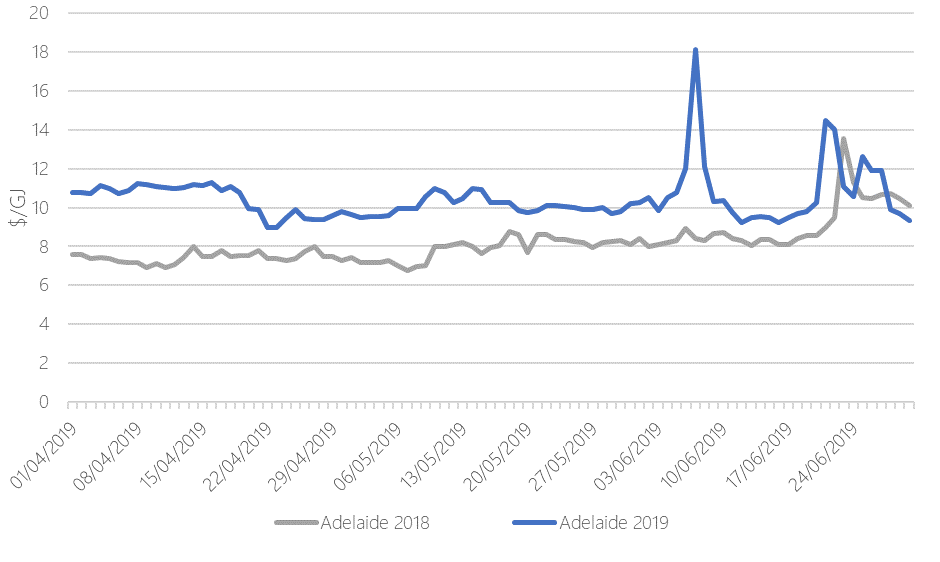

Adelaide

Adelaide Q219 average STTM price was $10.45/GJ which was $2.29/GJ higher than the Q218 average price. Sustained higher prices as well as a spike during June contributed to the higher average price.

(Source: AEMO)

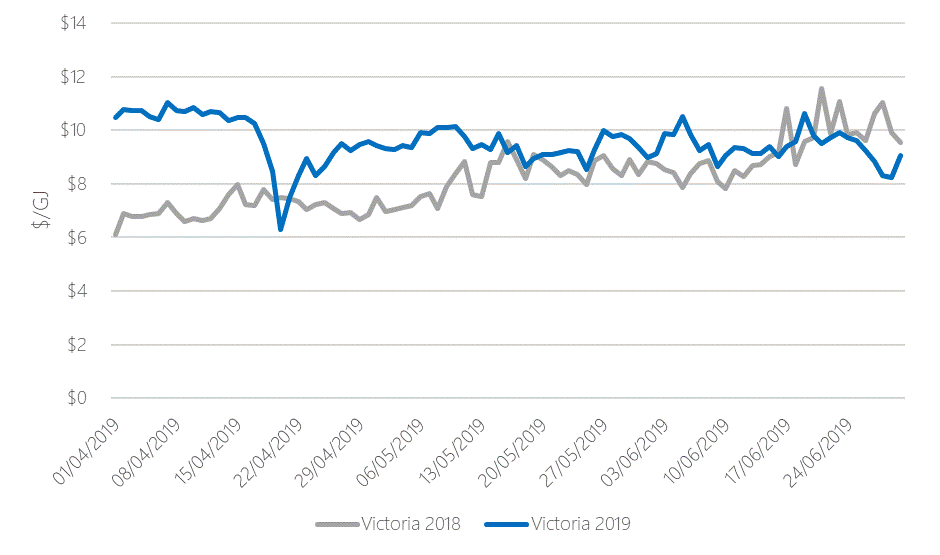

Victoria

Victoria Q219 average gas price was $9.54/GJ which was $1.36/GJ higher than the Q218 average price. Prices were higher earlier in the quarter then converged in May. In late June gas prices softened, potentially on the back of less demand from electricity generators due to high wind.

(Source: AEMO)

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220.