In a surprise outcome the LNP maintained leadership over the weekend noting that it remains unknown whether or not the LNP will form a majority government. Energy and climate were at the heart of this election with Labor putting forward material initiatives that would increase investment in renewable energy generation (increased funding to the CEFC) and reduce emissions through the extension of the safeguard mechanism, amongst a number of other initiatives. The LNP are less ambitious and maintain the emissions reduction target of 26-28% below 2005 levels by 2030. The LNP will extend the Climate Solutions Fund by providing additional funding to the Emissions Reduction Fund which is the reverse auction of ACCU’s managed by the Clean Energy Regulator.

In terms of energy generation and transmission the LNP has pledged

support for Snowy Hydro 2.0, the Underwriting New Generation Investment program

and Marinus Link (Interconnector between TAS and VIC, part of the Battery of

the Nation plan).

The futures markets (energy and environmental certificates) had priced in a Labor victory. The result over the weekend may put upward pressure on forward prices (energy & Enviro) as there will be less new renewable generation invested in over the coming years. That being said, state based renewable energy targets remain in place as per the following:

QLD – 50% Renewable by 2030

NSW – No target

VIC – 25% by 2020 and 40% by 2025

SA – No target

Tas – 100% by 2022

The larger demand states are QLD, NSW and VIC who are still heavily reliant on coal powered generation. NSW is the only state of these three whereby there is no target. Given that QLD and VICs renewable energy targets remain in place there should not be a material decline in new renewable generation development in these regions. For NSW, at least for the time being, new renewable generation will be a function of price. Currently NSW prices are at a level whereby a solar or wind developer should be able to secure funding and a PPA.

If you would like to know more about the potential impact that our LNP government may have on Australian energy prices, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

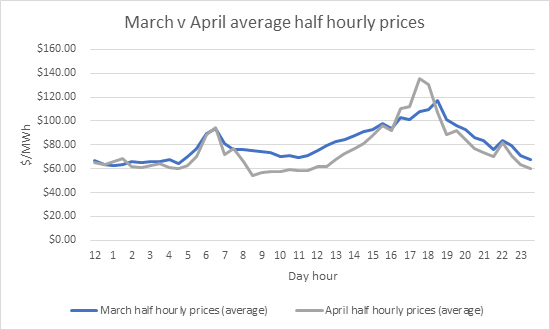

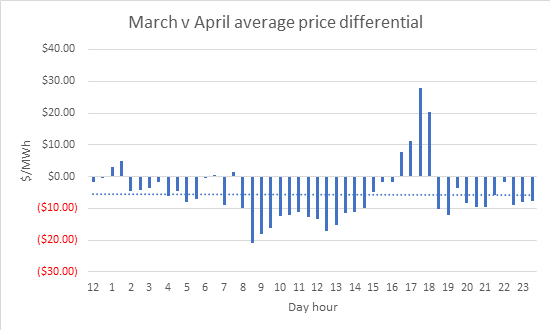

In Queensland, we have observed lower daytime spot prices since the beginning of April, relative to March averages.

Taking a closer look at half hourly average spot prices seen so far in April, we can see that between 8am and 4pm spot prices have been softer than the same periods in March. Following this, spot prices are higher in the evening peak periods. Whilst it is a very small data set, this is the relationship that many in the market expect to evolve.

Softer spot prices in the day will motivate generators to

price more aggressively (price higher) in the evening peak to increase earnings

which have been lost during the day.

Should we see this evolution of softer spot prices during the sunlight hours of the day, it will put further strain on the Queensland solar industry which has had several setbacks of late.

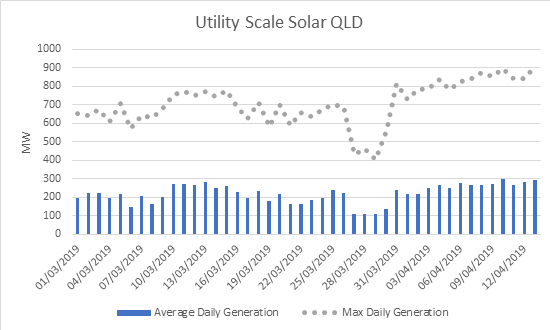

In addition, we can observe from the below graph that there has been an increase in generation from utility scale solar, in terms of both peak and average generation. The increase in solar is making more low-cost generation available in Queensland. New generation from these solar plants remains insufficient to meet all demand and therefore, solar is not setting prices.

If you have any questions regarding spot prices or any other matter relating to energy, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

Alex Driscoll, Manager Wholesale Clients and Markets

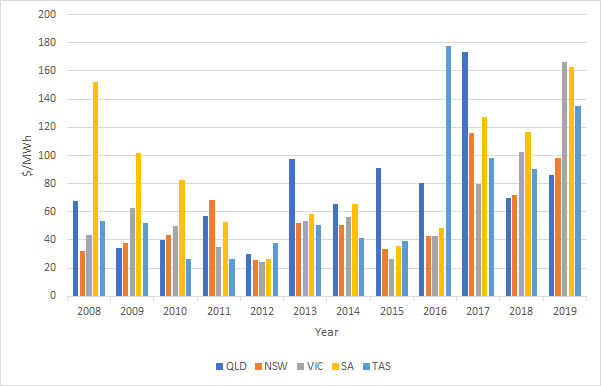

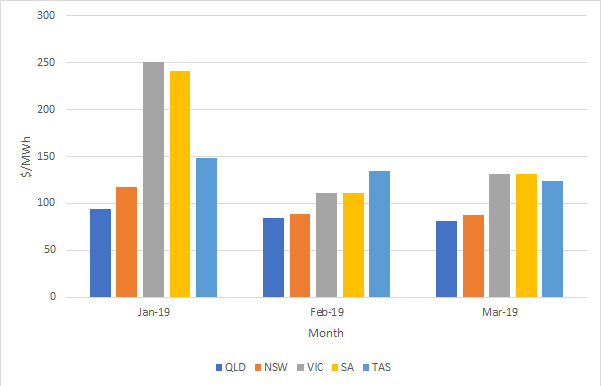

The electricity spot prices were higher for the Summer period (January – March) compared to the preceding three months. Although demand remained static, prices increased as a result of coal and gas generation setting prices at elevated levels. Average prices increased in all regions from the previous summer, with Queensland increasing the least at 23% and Victoria increasing the most at 62%.

Across all regions, prices during the 2019 summer were higher than the 2018 summer and were very high in a historical context for Victoria, South Australia and Tasmania. Looking back across the last 10 summers, 2019 summer prices are at their highest levels in most states.

Figure 1: Historical prices for summer

It should be noted that prices in both 2012 and 2013 were affected by a carbon tax, which was subsequently repealed in 2014. Since then, there has been a steady price increase in all mainland NEM regions. In Queensland, the Government provided a direction to Stanwell Corporation and CS Energy to adopt strategies to reduce wholesale prices. Since the direction, there have been fewer price spikes (prices above $300/MWh), although average prices have continued to increase.

Price spikes in late January for NSW, South Australia and Victoria were driven by a combination of the following factors:

the lack of wind generation;

reduced limits on interconnectors;

reduced thermal generation output; and

hot weather increasing demand.

High temperatures also increased demand for Queensland in mid-February, pushing demand to 9,988MW.

The New South Wales market was relatively stable over summer with limited volatility. Throughout the season, prices only spiked above $500/MWh for the trading interval on 2 occasions. Snowy Hydro continues to draw down its dam levels to cover cap contracts and supress prices below $300/MWh.

Quarter 1 2019 saw a lower level of generation for gas powered generators as a result of the increased level of generation from renewables and the rising cost of fuel. Renewable generation continues to grow to over 3GW from the start of the year. Operational demand dropped to its lowest level since 2002 as a result of a reduction in energy intensive industries and the increased uptake in rooftop solar PV.

Figure 2: Average monthly spot prices in the NEM

Coal fired generation was at its lowest level since the start of the market on 13 December 1998. This lower level of generation was driven by prolonged outages at Yallourn and Loy Yang A and the increase in market share from renewables. Coal fired generation was also impacted by an increased number of trips, increasing from 10 in the previous quarter to close to 30 in Q119.

Hydro generation was reduced driven by lower dam levels or water conservation strategies by Snowy Hydro in New South Wales and Victoria, and Hydro Tasmania in Tasmania.

Looking forward

Higher spot prices and concerns over the stability of the grid have caused the forward curve to increase. Snowy Hydro continue to draw down on its dam reserves and with a dry outlook, the inflows could be lower than previous years. If Snowy Hydro reduce output during 2019, spot prices could be even higher than current prices.

There is currently a huge pipeline of committed projects waiting to enter the market. These projects are mainly renewable energy, diesel and batteries. The integration of renewable energy generation into the market and the strategies of price setting coal and gas generation will determine if prices will reduce or if a more volatile market will be created. It is unlikely in the near term that spot prices will return to historical levels as renewable generation has not reached the volume required to consistently set prices at lower levels.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Manager Wholesale Clients and Markets, Alex Driscoll on 07 3905 9220.

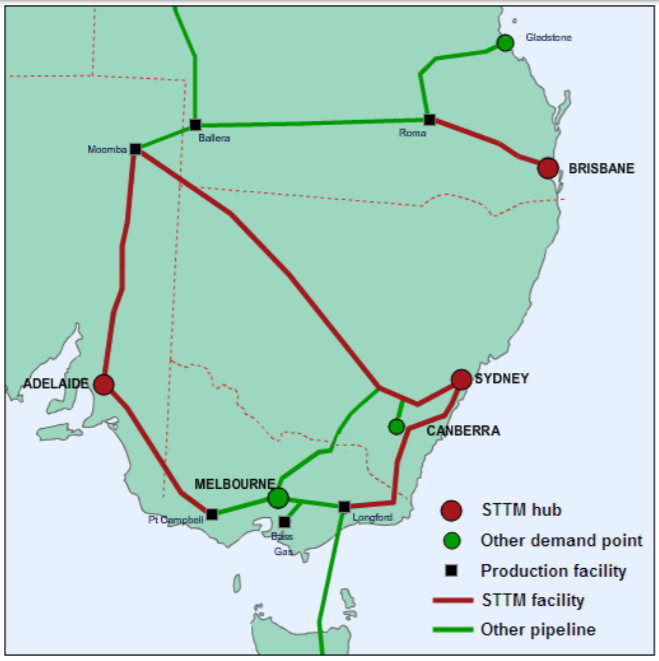

For a growing number of large energy consumers, consideration is turning to whether entering standard vanilla retail gas agreements deliver the most effective outcome. For consumers who are located within the bounds of the Sydney, Brisbane or Adelaide Short Term Trading Market (STTM) markets, many may not be aware that there is an alternative way to purchase gas. Below, we consider how the STTM works and what the benefits are of exploring this option.

What is the STTM

The STTM is essentially a market for the trading of natural gas at a wholesale level at defined hubs between pipelines and distribution systems. The STTM is a day-ahead gas market operated by the Australian Energy Market Operator (AEMO) with hubs located in Sydney, Adelaide and Brisbane. This means that gas is traded a day ahead of the actual gas day. The market settles daily with “shippers” delivering gas and “users” consuming gas. An organisation may sell gas as a shipper and purchase gas as a user through the same STTM, however, it would do so at the daily market price.

Source: “Overview of the STTM for Natural Gas”, AEMO, page 1

Market participants are incentivised to ship and consume volumes of gas nominated through a pricing mechanism, which aims to keep the gas supply system balanced. Organisations are able to sell excess gas to its requirements on the open market the next day, as well as bid to purchase extra gas as and when required. This system allows participants more flexibility and choice in purchasing gas supplies. Furthermore, the STTM’s price transparency ensures that the price set by the market daily truly reflects the current supply and demand situation.

Each of the STTM hub settles independently of the other, however each hub operates under the same rules outlined by AEMO.

There are a range of drivers for some large gas consumers transitioning to purchasing and selling gas in the STTM. The main reasons are:

The STTM is an historically lower commodity cost;

Consumers can manage or avoid penalties under daily, monthly, and / or annual take or pay positions;

There is increased flexibility for both sellers and consumers; and

There are no long-term commitments.

These benefits can materially lower the cost of consuming gas. Depending on the nature of the organisation, there are a range of structures to access an STTM. Each structure requires varying levels of engagement from the consumer.

Engagement with Edge

To assist in transitioning your organisation to accessing the STTM, Edge are able to offer the following services:

Daily nominations and trading;

Monthly reconciliation;

Facilitation of short and long-term Gas Supply Agreements; and

Managing the STTM application.

Entering the STTM market is strategic decision for most organisations and can take anywhere between 3-12 months to transition. If you would like to know more, please contact us to understand if accessing the STTM market is the right decision for your organisation.

We note that there are also alternatives for consumers who are not within the STTM limits, however these options are not discussed for the purposes of this article. If you would like further information on your options, please contact your Manager Wholesale Clients or Edge on (07) 3905 9220.

As of 1 March, the new Capacity Trading Platform (CTP) and Day Ahead Auction (DAA) came online. This market arose after the Council of Australian Governments (COAG) Energy Council agreed to implement the legal and regulatory framework required to give effect to the capacity trading reform package, as recommended by the Australian Energy Market Commission (AEMC) as part of its Easter Australian Wholesale Gas Market and Pipelines Framework Review.

The reforms apply to the operators of transmission pipelines and compression facilities operating under the contract carriage model (collectively referred to as “transportation services”). The objective of the reforms is to encourage and facilitate trading of unutilised capacity on non-exempt transportation facilities. This is achieved by providing shippers with an incentive to trade spare capacity on a secondary capacity market (the CTP). If a shipper fails to sell any spare capacity prior to the nomination cut-off time, then its contracted but unnominated (CBU) capacity is then offered to other participants in an auction conducted a day ahead of the gas day (the DAA). In contrast to trades conducted by shippers prior to nomination cut-off time, the proceeds from the auction are retained by the service provider, which incentivises shippers to sell their spare capacity ahead of nomination cut-off time. (AEMO, Pipeline Capacity Trading: Overview, 2018).

According to the Australian Energy Regulator (AER) in the first two weeks of the DAA, 1.87 PJ of capacity was bought across multiple pipelines and compressors (Australian Energy Regulator, Gas Market Report, March 2019).

C&I Gas pricing

C&I gas contracts continues to be an opaque market. Contract prices have softened since the peak in 2016, however remain high and continue to put businesses under strain who are challenged with either absorbing higher costs or passing these onto customers.

AEMO recently released their Gas Statement Of Opportunity which reinforced the situation that domestic gas supply and demand balance is tight. AEMO highlighted that:

“Supply from existing and committed gas developments is forecast to provide adequate supply to meet gas demands until 2023. However, risks remain that any weather-driven variances in consumption or electricity market activity could increase gas demand, creating potential peak-day shortages as outlined in AEMO’s 2019 Victorian Gas Planning Report”.

Weather driven variances in consumption were observed in late January this year when the Cumulative Price Threshold was met and the Administered Price was activated VIC and SA. This highlight from AEMO is generally concerning as it suggests that there is unlikely to be any reprieve in gas prices in the near to medium term.

Recently, pricing for C&I customers has been observed between $11.00/GJ and $14.00/GJ subject to terms and conditions. Customers are increasingly looking at taking on more responsibility for their consumption in an effort to bring down the commodity price.

Gas Powered Generation

Gas powered generation in Q119 was 4% higher than Q118 with less generation from hydro, black coal and brown coal. There was a material increase in generation from solar and wind resources which was to be expected.

Average prices in the STTM hubs and the VIC gas market all increased in Q119 relative to Q118. Volumes were lower in the STTM markets, whereas the volumes increased through the VIC market. Gas fired generation in VIC averaged 75TJ/day in Q119, which was 23TJ/day higher than Q118. Less generation from brown coal and hydro generators was the primary driver behind this.

Regional analysis

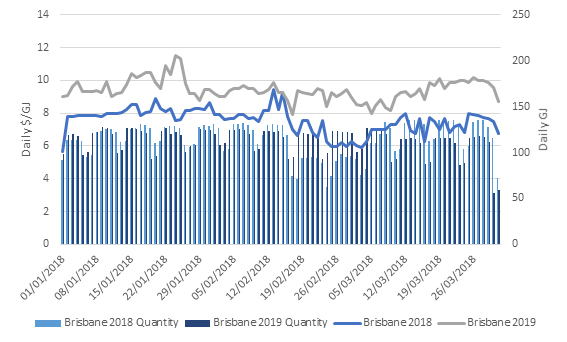

Brisbane

Brisbane STTM gas prices were higher in Q119 relative to Q118. Prices were consistently higher and generally followed a similar pricing trend. Volumes exchanged through the STTM were marginally higher in Q118 relative to Q119.

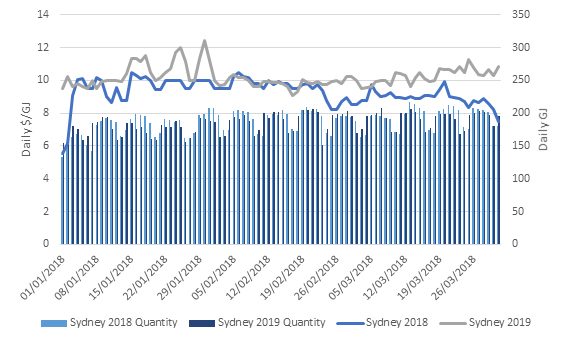

Sydney

Sydney STTM gas prices were higher in Q119 relative to Q118 with a divergence in prices in the final week of the month. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

Adelaide

Adelaide STTM gas prices were higher in Q119 relative to Q118. Q119 prices were consistently above that of Q118, with the exception of a few days at the beginning of February. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

Victoria

VIC gas prices were higher in Q119 relative to Q118 with prices diverging in the final weeks of the quarter. Unlike the STTM markets, there was more volume traded through the VIC market in Q119 relative to that of Q118. On the 24th and 25th of January, there was a spike in gas volumes which was driven by higher demand from the Gas Powered Generators as a result of very high electricity prices.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220.

On 12 March 2019, the Clean Energy Regulator (CER) has confirmed the 2019 renewable power percentage (RPP) and small-scale technology percentage (STP) has been set by legislative amendment.

The 2019 RRP has been set at 18.6% and the 2019 STP has been set at 21.73%.

As explained by the CER, the RRP and STP set the annual statutory demand for large-scale generation certificates and small-scale technology certificates in the Renewable Energy Target.

If you have any questions regarding the 2019 RRP or STP or any other matter relating to energy, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

The Australian Energy Market Operator (AEMO) released its draft marginal loss factors (MLFs) today. As generally expected, solar and wind farms that are a long distance from the regional reference point have been hurt.

The most notable example of this is the Broken Hill solar farm, which has a draft MLF for FY20 of 0.7254. This is 0.2535 below the current MLF. If the draft MLF is confirmed in the final report (due 1 April 2019), this will reduce the volume of electricity sold by the solar farm by 25%.

A number of other solar and wind farms had material reductions in MLF and are facing a challenging situation. Most notably, Silverton Wind Farm (NSW), Karadoc Solar Farm (VIC), Griffith Solar Farm (NSW) and Parkes Solar Farm (NSW).

MLFs are very difficult to estimate, which is reflected in the relatively large change we are observing year on year. Amongst many other concerns, this creates uncertainty for the investment community.

If you have any questions regarding the draft MLFs or any other matter relating to energy, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

With expectations that CleanCo will be trading in the NEM by mid this year, things are getting into full swing. Last week CleanCo appointed its first two key executives – Miles George and Geoff Dutaillis.

Who are these new executives?

Miles George has been appointed the Interim Chief Executive Officer (CEO) at CleanCo. His role at CleanCo is to secure cleaner, more affordable, sustainable energy and secure supply of electricity for Queensland (QLD). He was previously the CEO and Managing Director of Infigen Energy. After leaving Infigen Energy in 2016, Miles continued as a strategic adviser until December 2017. During and after his time at Infigen, Miles has been the Chairman of the Clean Energy Council, a representative on the AEMC Reliability panel, an Expert panel member for AEMO and Director of the Australian Conservation Foundation.

Geoff Dutaillis has been appointed the General Manager of Transition. Geoff was most recently the CEO (Australia) of Wind Energy Holdings, a leading renewable energy company based in Thailand. The company has interest in various Australian wind farms. Geoff has also held executive positions at Infigen Energy as Chief Operating Officer (COO) from 2009 until 2013 and Lendlease more recently as Head of Sustainability.

What is the mandate for CleanCo?

CleanCo has the mandate to increase competition in the electricity market at peak times of demand when prices are generally at their highest. CleanCo is expected to transform intermittent renewable generation into firm financial products for customers and retailers while backing QLD’s renewable energy and low emissions generators.

Which of the existing generators are to be transferred from the current government owned corporations; Stanwell and CS Energy?

Initially, CleanCo’s portfolio will include a range of existing renewable and low emission energy generation assets including:

Wivenhoe pump storage hydro plant,

Swanbank E gas-fired power station, and

Barron Gorge, Kareeya and Koombooloomba hydro power stations.

If you have any questions regarding CleanCo or any other matter relating to energy, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

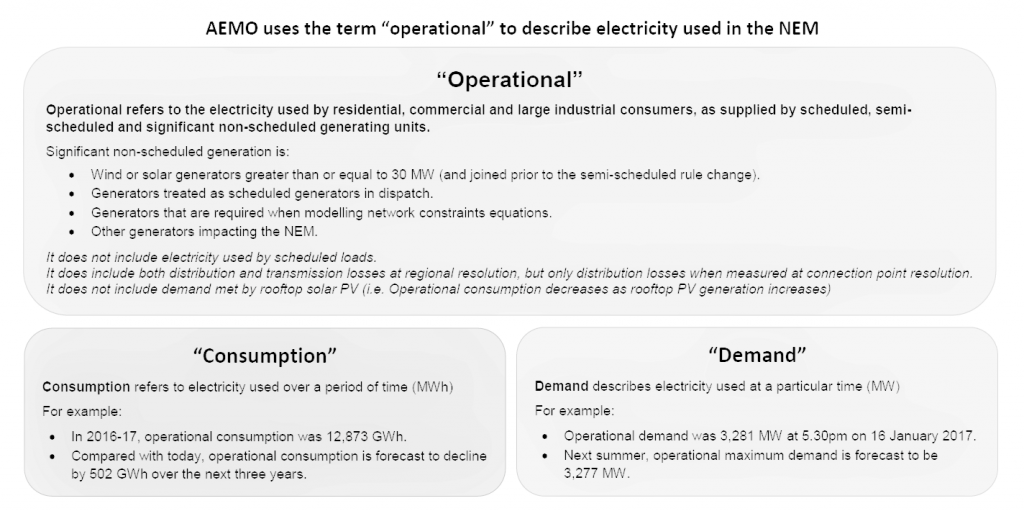

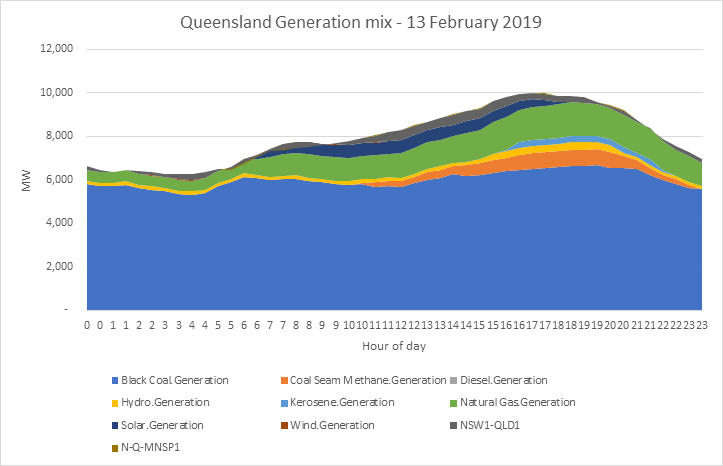

Queensland (QLD) operational demand (see definition in image below) reached a new all-time record of 10,052 MW at 4.55pm yesterday (13th February 2019) largely as a result of temperature driven demand. Despite record demand, spot prices remained steady with QLD generators ramping up generation and conservative bidding from key generators.

Image sourced from AEMO

In terms of what type of generation was keeping the lights on, black coal and gas were the two largest contributing fuel sources (as shown in the image below). At the time of peak demand, 6,458 MW of generation was coming from coal and 2,253 MW from gas (natural gas and coal seam gas).

Should demand have crept even higher, Wivenhoe pumped storage

hydro still had capacity to ramp up generation to maintain stable pricing.

If you have any questions regarding this article, please contact Edge Energy Services on 07 3905 9227.

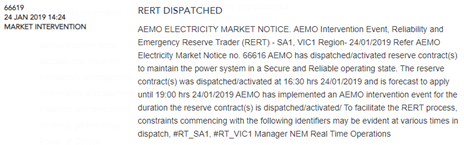

Edge Energy Services recently published an article on the 16th of January outlining what happens in the market when high prices and a lack of reserves are published in pre-dispatch. On the 24th January, it was a different story, where extreme temperatures and high demand in South Australia (SA) lead to load shedding, activation of RERT and operation of the emergency generators in SA. This resulted in the maximum price reaching $14,500/MWh with an average of $3,388/MW.

At the start of the week the Bureau of Meteorology forecast high temperatures across SA and Victoria (VIC) for the coming week. On the morning of the 23rd January, AEMO flagged extreme temperatures for SA and VIC and requested participants to update generation levels inline with expected conditions.

High temperatures and humidity have significant impacts on:

Performance of gas-powered generation and;

Energy usage of end users resulting in high demand levels.

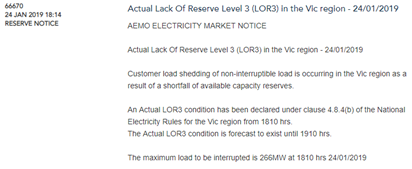

In addition to extreme temperatures driving high demand, the loss of a Loy Yang A unit earlier in the week due to a tube leak. The reserve levels within VIC then fell to a point where LOR3 (Lack of Reserve 3) was activated. When LOR3 is activated, load shedding occurs.

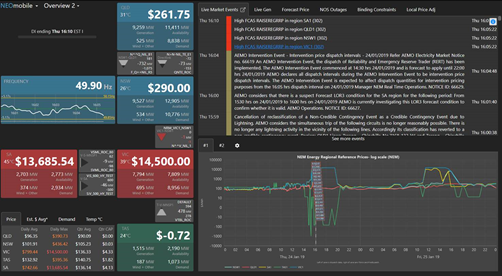

At 15:00 an IRPM (Instantaneous Reserve Plant Margin) of 8% for the SA and VIC economic island was calculated. This indicated there was only 881MW of spare capacity in the islanded region. This information formed part of a report published by Global-Roam.

At 16:14 AEMO published a market notice stating a LOR3 had occurred and load shedding had commenced at 16:10. Changes in demand indicated 266MW of load was shed. The supply / demand balance changed during the day and reached levels where the LOR3 could be cancelled at 20:00.

Prior to load shedding, AEMO activated RERT (Reliability and Emergency Reserve Trader) at 14:24 which involves a combination of voluntary load shedding and demand side management. RERT was activated from 16:30 until 19:00.

During high price periods, most generators were operating at close to maximum capacity. The SA Emergency generators also ran between 17:00 and 21:15 adding 200MW to the grid. This volume assisted VIC via the interconnector flows. Wind resources were low in VIC and neighbouring regions, resulting in less than expected generation

The constraint N^^V_NIL_1, which effects the limit of capability through the NSW-VIC interconnector also bound resulting in a limit of supply to the region from Queensland (QLD) and New South Wales (NSW).

As a result of all the factors mentioned above, the spot price in VIC stayed at close to $14,500/MWh from 15:00 to 21:30. The diagram below highlights the resulting price, flows and regional prices for a 5 min interval of the day.

As a result of the high prices in VIC, the spot price for the quarter to date is currently $276.77/MWh compared with $119/MWh before Thursday.

Current contract prices for VIC are around $140/MWh for quarter 1 of 2019. Given these higher prices, users with existing exposure to the spot price would have been significantly better off if they were highly contracted. End users with the ability to change their exposure via demand side management would also have benefited from reducing demand.

As a result of the volatility yesterday the administrative price cap has been activated from 11:30am today. This will apply until prices decline below the price administered threshold.

If you have any questions regarding this article or the electricity market in general, call Edge on 07 3905 9220 or 1800 334 336.