ARENA has released their public summary of the Request For Information (RFI) on Concentrated Solar Thermal (CST) projects. The RFI process was designed to examine the potential for a possible program supporting the deployment of CST systems in Australia. There were 31 respondents to the RFI. Respondents ranged from the most experienced in the world to relatively junior Australian companies. There were a couple of key takeaways from the exercise which included:

– That dispatchable and flexible generation coupled with synchronous generation was beneficial;

– Cost discovery was limited as pricing is commercially sensitive in nature. More junior developers offered low pricing;

– There are a number of regulatory, commercial and technical challenges to CST.

– Long development time relative to solar PV

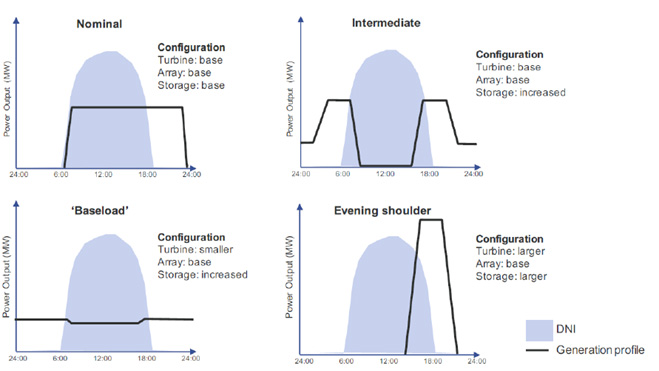

Image 1 comes from Vast Solar and was included in the ARENA report. The image provides a summary of the generation capability of a CST. Noting that the profile is a function of the physical design.

Image 1. CST potential generation profile

Source: Synthesis of Responses to ARENA’s 2017 Request for Information on CST and Vast Solar

The information collected on pricing was limited however, ARENA did provide a Levelised Cost of Electricity (LCOE) estimate based on 12 of the respondents RFI’s. The lower estimate was $124.00/MWh and upper was $154.00/MWh. These numbers are significantly above the reported price of $78.00/MWh that the SA Government is paying for generation from the Port Augusta CST plant (noting there is a significantly discounted loan attached to that project).

Concentrated Solar Thermal and the National Energy Guarantee?

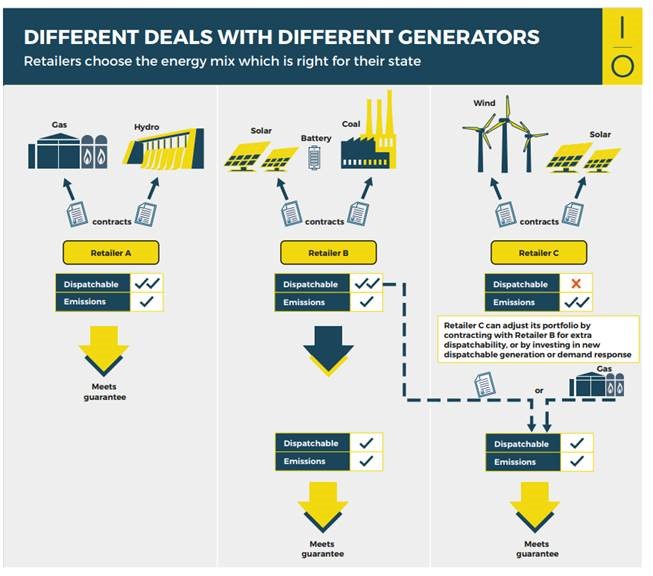

At a high-level CST appears to be the golden egg of generation assets if the NEG is implemented. The assets are renewable and dispatchable which positions itself to be able to write dispatchable and low emissions contracts (Image 2.). The question is will the incentives under the NEG be sufficient to warrant the price and risks associated with CST. Currently, the answer seems to be no. The answer is no because of the considerable uncertainty around how the NEG will function and the developers ability to forecast income.

The timeline for the NEG is tight, when asked earlier in the week the ESB Chair Kerry Schott referred to the time frame as “tight but doable”, an underwhelming response. Vague language of this nature does not signal confidence to the investment community nor the consumer. In addition to this, the Federal opposition has been quiet on where they stand in respect to the NEG. In the near term, we are unlikely to see investment in large-scale CST until further clarity is provided on the NEG.

Image 2.

Source: Energy Security Board

Edge maintains strong relationships with developers of CST plants. If you are interested in understanding more, please get in contact with us. For further information on the National Energy Guarantee please follow the link to our recent submission.

If you would like to know more about energy costs and state-based subsidy, please get in contact with Edge on (07) 3905 9220 or 1800 334 336.

The new South Australian Premier, Steven Marshall, will be looking to reduce energy prices in the state.

Mr Marshall is not in favour of setting a state-based target for renewable energy and has noted that even without a target, the state is likely to reach 74% of all electricity being renewable in 2025 and 76% in 2030.

Mr Marshall is focusing on batteries and additional interconnection instead. He is aiming to establish a fund within his first 100 days in office to provide a $2,500 subsidy for up to 40,000 household to purchase a battery. The subsidy will be available to households that already have solar PV and will be means tested, however the exact details around qualifying for subsidy is yet to be released. ElectraNet is already exploring options for additional interconnection with the rest of the market. The State Liberal Party will assist with a $200 million inter-connection fund designed to speed up the process of making a final decision.

Finally, the new State Government is looking at options for the new fast-start gas plant which the previous government committed to. The Liberal Government is not in favour of adding it to the market however they admit that they are not sure what options they currently have.

If you would like to know more about energy costs and state based subsidy, please get in contact with Edge on (07) 3905 9220 or 1800 334 336.

Together with the National Greenhouse and Energy Reporting Act 2007, the safeguard mechanism provides a framework for Australia’s largest emitters to measure, report and manage their emissions. It gives businesses a legislated obligation to keep net emissions below their baseline. Baselines are intended to accommodate business growth and allow businesses to continue normal operations.

The Clean Energy Regulator recently released the first full year of data on 14 March 2018 under the safe guard mechanism.

The safeguard mechanism commenced on 1 July 2016, with the first reporting period ending 30 June 2017. Emissions were reported to the Clean Energy Regulator as part of the National Greenhouse and Energy Reporting scheme on 31 October 2017. Responsible emitters had until 28 February 2018 to surrender Australian carbon credit units (ACCUs) if their emissions were above their baseline.

The Clean Energy Regulator is required to publish information about all large facilities with emissions over 100,000 tonnes of carbon dioxide equivalent (CO2-e) for each reporting year.

As at 31 October 2017, there were 154 responsible emitters identified with one or more large facilities, resulting in 203 facilities having legislated obligations under the safeguard mechanism for the 2016–17 reporting year.

Clean Energy Regulator Chair David Parker announced that all responsible emitters have met their requirements in the first full year of the safeguard mechanism. Of the 154 emitters there were 3 companies that withheld information which is allowable under section 25 of the National Greenhouse and Energy Reporting ACT 2007 if the organisation is protecting trade secrets or commercial information.

There were 16 companies that exceeded their baseline and were required to surrender carbon credit units.

If your company requires brokerage services for carbon units please get in contact with Edge on (07) 3905 9220 or 1800 334 336.

By Thomas Dargue, Edge Manager of Markets & Advisory

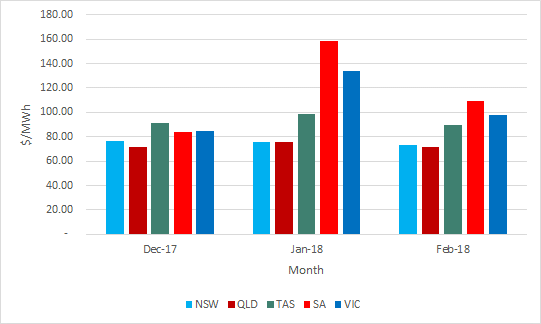

In this summer edition of the market update we look at some of the issues which is causing price differences in wholesale prices across the east coast of Australia. Since the start of summer, the divide has mainly been across the Murray river with QLD and NSW to the north and VIC, SA and TAS sitting to the South.

The summer started in December with modest spot prices across all the regions. The region with the highest price was TAS at $90.96/MWh with the lowest price being QLD at $76.56/MWh. The interconnectedness of the market means that prices in NSW was similar to QLD while SA and VIC were closer to TAS. The prices in NSW started deviating from the southern market as the interconnector with VIC became increasingly constrained. Throughout January there were large price spikes in SA and VIC increasing the average price south of the Murray. The constrained interconnector meant that the prices never travel north and both QLD and NSW had modest prices.

Figure 1 Average NEM spot prices.

Tasmania had similar prices throughout the three months however these seem to be too high for the State Liberal Government. There is an election in Tasmania 3 March 2018 and one of the policies put forward by the State Liberal Government would be a split from the NEM. TAS would still be physically connected through Basslink however would not be subject to the price setting mechanism set out for the NEM. The State Liberal Party is expecting this to result in lower wholesale prices for TAS.

Prices for summer to date has been higher in SA than any other state however there haven’t been any black outs. This is in part due to the operation of a new 100 MW battery installed by Tesla which provides energy during peak times as well as support for frequency. With an election in SA 17 March 2018 the incumbent State Labor party made its own electricity policy announcement. It would seek to further partner with Tesla to install 50,000 rooftop solar panels and batteries. When combined this would create a virtual 250 MW power station.

The Energy Security Board (ESB) realised its Draft Design Consultation Paper on the National Energy Guarantee (NEG). The NEG seek to find a balance between affordability, reliability and carbon reduction which could be politically acceptable. With the number of schemes already rejected by the Federal Government, the ESB has managed to come up with a scheme which could get bi-partisan support. At this stage there is quiet optimism however there are large concerns over the effect on contracting going forward. The ESB is looking for written submissions by 8 March 2018 and have the final design by the second half of 2018.

The forward prices generally reduced for 2019 as spot prices were less volatile than seen in previous years over summer. The exception was SA where there is still uncertainty around security of supply.

Table 1: ASX prices for Calendar Year 2019

NSW

QLD

SA

VIC

1 DEC 2017

80.75

68.11

92.94

86.55

28 FEB 2018

76.38

64.03

94.36

82.90

The forward prices were lowest in QLD where we expect a large amount of new renewable generation to be built. Concerns over sufficient supply in other regions kept prices higher.

Despite higher forward prices and the highest average spot prices in the NEM, a hydrogen electrolyser will be built in Port Lincoln, South Australia. This will produce hydrogen using excess wind and solar (i.e. when prices are low) to produce hydrogen both to power a 10 MW gas turbine but also for export purposes. By using power intermittently, it is able to ramp up during low prices and not run during high spot prices which will also stabilise the grid and allow more wind generation to be dispatched in the region (wind in SA is currently being curtailed by AEMO to avoid frequency issues). It seems counterintuitive to put an energy intensive industry in SA however for very flexible consumption of electricity who are able to take advantage of low, or even negative, spot prices there is opportunity in the state.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact Thomas on 07 3905 9226 or on 1800 EDGE ENERGY.

The ACCC released the second interim report into gas supply arrangements in December 2017. In the initial report (released September 2017) it was reported that there would be shortages in gas supply available to east coast consumers in 2018. The report found that buyers of gas were receiving offers from a reduced number of suppliers and that prices offered were above the ACCC’s benchmark prices. It was also noted in the report the lack of participation from the QLD LNG producers in the domestic market. This reported lack of participation from the LNG producers prompted the Federal Government to act. The result was the creation of a Heads of Agreement with the LNG producers which would see additional gas allocated to the domestic market. According to the second Interim Report (released in December 2017), since September 2017 the QLD LNG producers contracted 42 PJ’s of gas under long-term supply agreements to domestic buyers for supply in 2018. The majority of this gas was sold to aggregators and retailers. The ACCC’s forecast for the balance of gas was also updated in the second interim Report and resulted in an improved balance of 75 PJ’s. The change in balance has been driven by a 12 PJ increase in supply and the lower demand from the LNG producers (63 PJ). Whilst on face value the market has gone from deficit to surplus, the balance remains tight and subject to gas producers meeting forecasts.

Table 1. Gas Balance

September Expected Domestic Demand Scenario (PJ)

December Expected Domestic Demand Scenario (PJ)

Supply

1,901

1,913

Domestic demand

642

642

LNG demand

1,314

1,251

Projected Balance

-55

20

Source: ACC Gas Inquiry Report – Second Interim

According to the report, there continues to be a shortage of production in the southern states to meet demand (SA, NSW, ACT, VIC and TAS). As a result, these states will continue to rely on gas transported from QLD. Additional costs to transport gas from QLD to VIC and SA are currently between $2/GJ and $4/GJ. Transporting gas south from QLD is not only expensive but due to limited firm capacity in key pipelines is not always feasible. Firm capacity in these key pipelines is predominately booked by the major retailers. It was examined by the ACCC if the major retailers were making spare capacity available to other users on major pipelines through secondary trading. It was found that on the major pipelines this was not the case however, there was some evidence to suggest this may have been occurring on the less critical pipelines. Since the ACCC investigation it has been observed that the retailers have increased the availability of spare capacity to other pipelines participants improving competition.

FIRM CAPACITY – The amount of transmission guaranteed to be available to the shipper – up to MDQ & MHQ every day

AS AVAILABLE CAPACITY – This capacity is typically spare contracted capacity that is offered on the secondary market. As can be disrupted or delayed, it is not necessarily guaranteed.

The ACCC expects that transportation costs will start to come down as regulatory reforms begin to take effect.

Domestic prices to large C&I customers were around $16/GJ in early 2017 and even higher for smaller business customers. Since July 2017, it was reported that prices between $8/GJ and $12/GJ were achieved by large C&I customers.

GAS PRICES

Across each of the east coast trading hubs January average prices were higher than the Q417 average.

Table 2. Hub Prices

Adelaide price ($/GJ)

Brisbane price ($/GJ)

Sydney price ($/GJ)

Melbourne price ($/GJ)

Q417

$7.14

$7.68

$7.12

$6.20

JAN18

$ 8.10

$8.16

$9.71

$8.64

FEB18

$9.29

$7.33

$9.71

$8.67

Source: AEMO

Recent news

Four projects have received funding from the South Australian Plan for Accelerating Exploration (PACE) gas program’s second round. The program was designed as part of a suite of measures to increase investment in local gas production and to ease price pressure in South Australia. The four projects to receive funding were:

$6.89 million for the Santos-Beach Cooper Basin project to deploy a heat-energy recovery system to offset natural gas used to run the Moomba petroleum processing plant

$5.26 million for the Senex Cooper Basin Gemba exploration/appraisal project

$6.89 million for Beach /Cooper Energy’s Dombey project in the Otway Basin

$4.95 million to the Rawson/Vintage Nangwarry project in the Otway Basin

Under the program, gas extracted through the PACE program must first be offered to local electricity generators, enhancing the affordability of supply. Whether the cheaper gas is passed onto end customers by the gas generators is more difficult to say.

Moving north to QLD, Senex’s 100% owned Western Surat Gas Project recently recorded a significant milestone, which was an all-in well cost of $1.2 million. The strong results have promoted Senex’s reputation in the market and has encouraged Project Atlas, which is another Surat Basin project expected to bring first gas in 2019, to be sold to the domestic market.

On 12 December Independent Scientific Inquiry into Hydraulic of Onshore Unconventional Reservoirs in the Northern Territory releases its draft final report. The overall conclusion of the report was:

“The overall conclusion of the Report is that risk is inherent in all development and that an onshore shale gas industry is no exception. However, if the recommendations made in this draft Report are adopted and implemented in full, those risks may be mitigated or reduced – and in many cases eliminated altogether – to acceptable levels having regard to the totality of the evidence.”

Since the release of the draft final report the panel has engaged with the Northern Territory community, Government, Industry, environmental groups, and other relevant stakeholders about the content of the report. This is the last opportunity for the Territorians to express their views on the inquiry.

The final round of regional consultations concluded mid-February and the final day for submissions due to the panel is 25 February 2018. At this stage the panel has committed to providing the Final Report to the government in March 2018.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220 or contact your Edge Portfolio Manager.

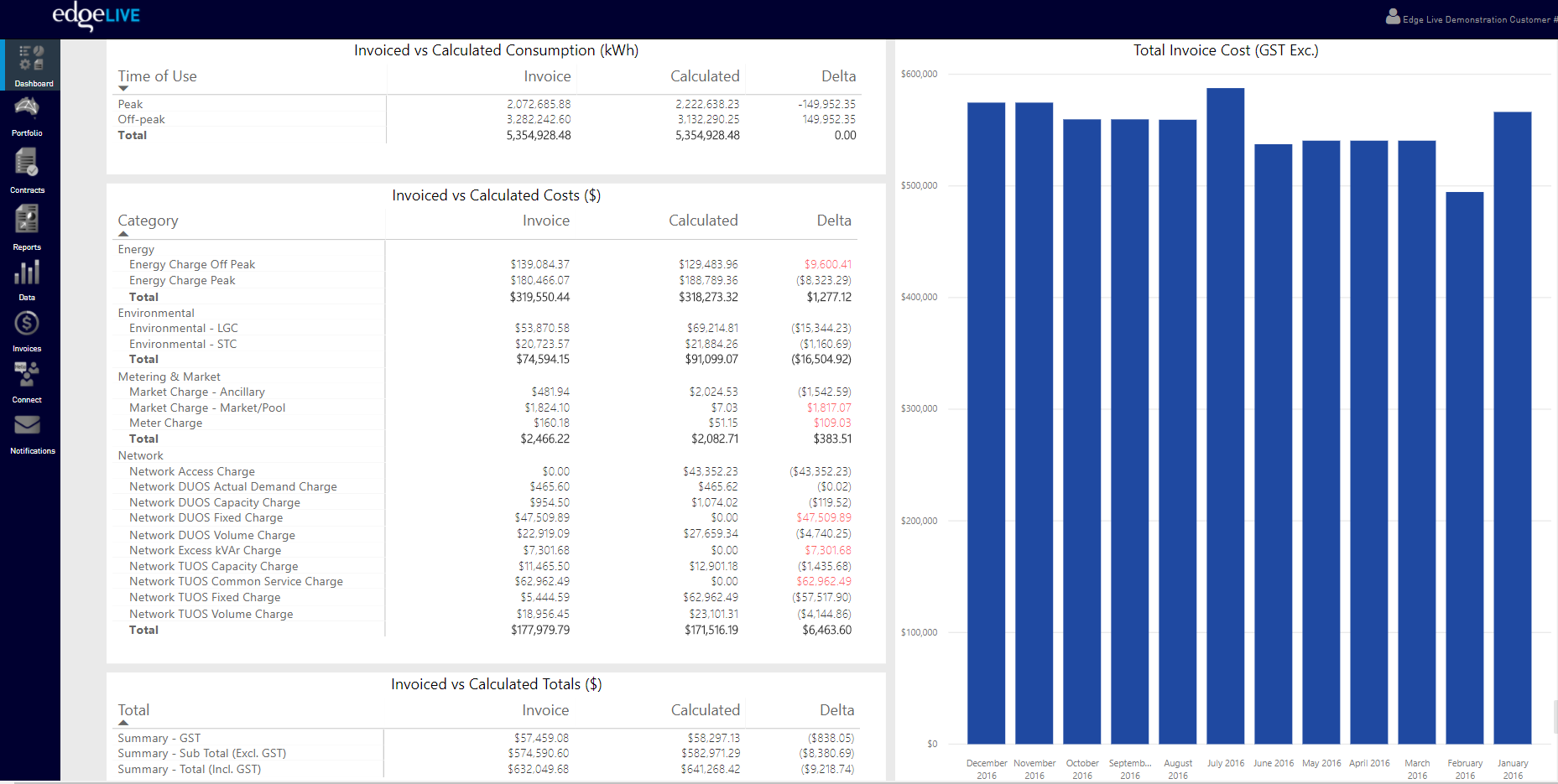

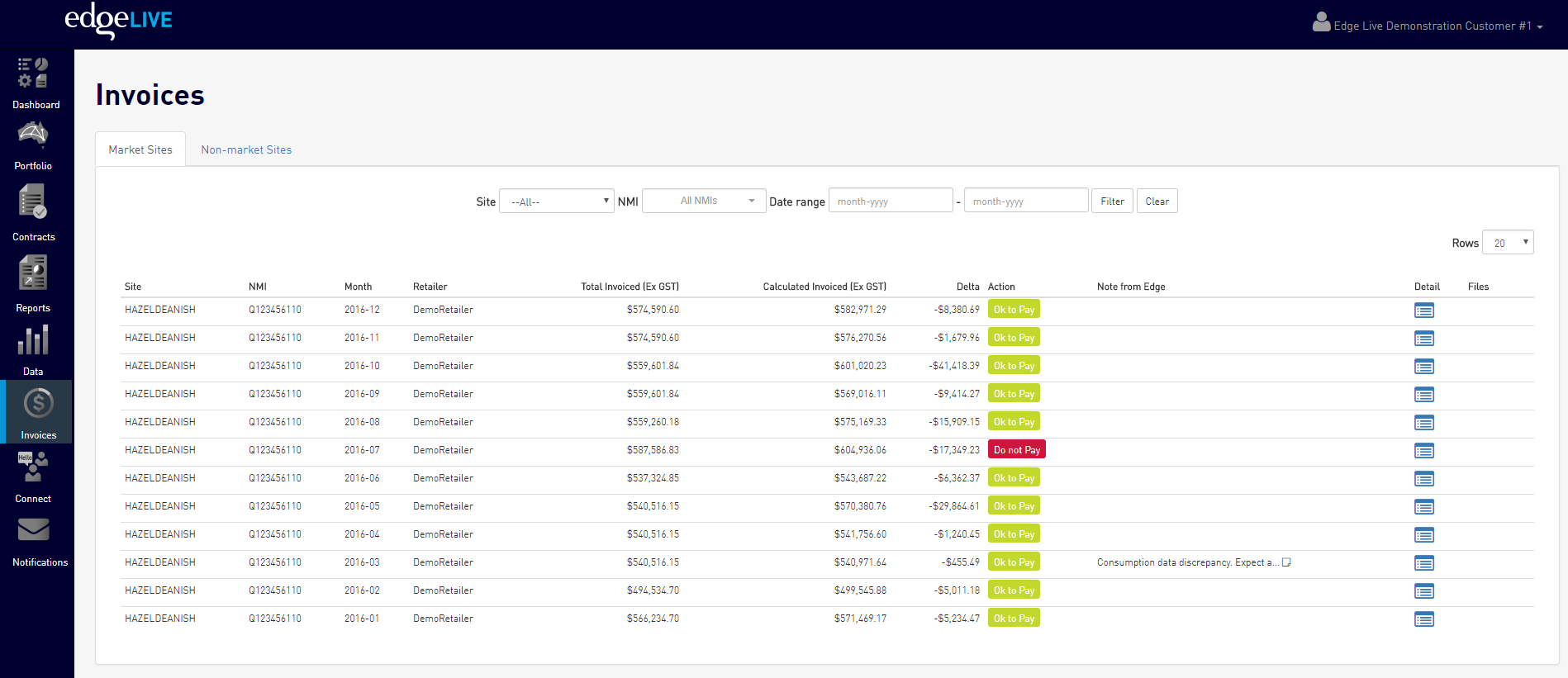

In addition to Snapshot functionality which provides you with information relating to your current and forecast spend and consumption, you can now access your Invoice Reconciliation and Accrual outcomes instantly within Edge Live.

Your Edge Portfolio Manager undertakes your Invoice Reconciliation services the same business day that your final invoice is issued by your Retailer. From here, the payment advice and outcomes are published instantly on Edge Live. You will receive an email notification that the reconciliation outcome is available, with links through to the Invoice Reconciliation Report. Providing you with details of the invoice outcome, broken down to the detailed levels of energy, network, markets and other costs.

Figure 1 Invoice reconciliation outcome in detail.

Viewing the results is easier and more efficient than ever before. View them in Edge Live directly from your web browser rather than having to open excel and find the information relevant to you. Though if you need to, the data can be exported to excel easily with the click of a button within Edge Live.

You will be provided with the invoice reconciliation outcomes, advice on whether to pay or not to pay and any additional personalised comments from your Portfolio Manager relating to your portfolio and individual sites.

Figure 2 Invoice reconciliation notification at an invoice level.

Your monthly Accruals reporting is also available via the online portal. Again, providing an easy and efficient way to advise your finance teams what the expected electricity spend of your portfolio will be as you near the end of each month.

And don’t forget about the existing Dashboard module. Filter by site and drill-down on specific time-frames of your electricity portfolio so that you can get a clearer view of consumption and costs.

Your Portfolio Manager will be in touch soon to discuss these new features with you, and ensure you have access to Edge Live as well as answer any questions you may have.

We have some exciting features planned for the remainder of 2018. If you have any feedback or suggestions on how Edge Live can be of more value to your business please do not hesitate to let us know, and we will do our best to incorporate this into our Edge Live development roadmap.

To learn more about Edge Live functionality click here, or speak with your Edge Portfolio Manager.

The first public consultation paper for the National Energy Guarantee (NEG) has been released today by the Independent Energy Security Board (ESB).

Dr Schott, the ESB Chair person said “The consultation paper seeks feedback from stakeholders on the high level design of the of the mechanism’s reliability and emissions component”.

The release of this paper is the first step in a consultation process that will occur over coming months. The ESB has advised that a high level design of the NEG will be provided to the COAG Energy Council in early April, ahead of a COAG meeting later that month when the report will be considered.

Edge will provide more details in the coming days. If you are interested in how the NEG will specifically impact your business or would like assistance with a submissions please get in contact with us.

The South Australian Premier, Jay Wetherill has announced that a deal has been made with Tesla to install 50,000 rooftop solar PV systems and Tesla batteries on homes in South Australia. The total capacity of the solar PV is expected to be around 250 MW or the size of a small power station.

The first 1,000 systems are already under way, being built by Housing Trust which is the South Australian Government’s low-cost housing arm. If successful, a further 24,000 government households will have the system installed, before being opened to private participation.

The details of the deal between the South Australian Government and Tesla is not known. Specifically, any success criteria to the first 1,000 installations and any cancellation clauses have not been disclosed. Cancellation clauses are particularly relevant given South Australia is facing an election on 17 March 2018. Prime Minister, Malcolm Turnbull, has warned against further experiments in the state’s electricity grid indicating that the Liberal party was unlikely to be supportive of a battery trial.

It is conceivable that a combination of batteries and solar PV may help to stabilise the local grid. The announcement by Mr Wetherill indicated that they would be looking for a retailer to manage the batteries. With a high correlation between low system security and low energy prices, retailers may have interest to dispatch the batteries when the energy prices are high, thereby mitigating their costs. Given the solar and battery system installations will be relatively small, they will not form part of central dispatch. This means that they cannot be relied upon by the Australian Energy Market Operator (AEMO) for system security. Control could be given to the distribution provider, who would be responsible for the low-voltage network instead of the retailer.. The distribution provider may want to dispatch the batteries at times of low prices to suit the network. This would reduce the revenue gained which would effectively make the pay back period on the batteries longer.

There is no doubt that the large battery installed by Tesla in South Australia has been a great publicity stunt for both the government and Tesla, however it would be interesting to understand which companies were invited to bid for the work and the selection criteria. There are a large number of Australian companies waiting to launch battery products at a large scale. Edge has previously reported on Planet Ark Power looking to reduce prices at Llewellyn Motors. Closer to Jay Wetherill’s home is Zen Energy and there are many other Australian companies wanting a chance to bid for a contract of this nature.

If you would like to know more about renewable energy projects and how they could assist with reducing your energy costs, please contact Edge on (07) 3232 1115 or 1800 334 336.

The Australian Energy Market Commission (AEMC) recently changed the rules governing electricity prices in the National Electricity Market (NEM). Instead of being paid on a 30 minute basis, the market will be paid on a 5 minute basis.

The main benefits of moving to 5 minute prices are greater participation of demand side management including batteries and less opportunities for gaming the market. For a full discussion see the AEMC website: http://www.aemc.gov.au/Rule-Changes/Five-Minute-Settlement

One of the main concerns over the change to 5 minute markets is that it will be difficult for traditional peaking plant to ramp up fast enough during high prices. Many of these peaking plants sell what is known as $300 caps which protects the buyer from prices above $300/MWh by paying the positive difference between the spot price and $300/MWh. As a price spike will only last for 5 minutes they are unable to capture the price in time and are no longer able to cover their position.

We saw a reaction from the Australian Stock Exchange (ASX) yesterday (22 January 2018) announcing that they would delist their caps starting 1 July 2021 when the new rule will take effect. It is uncertain what this will do to the business model of open cycle gas turbines and other peaking plants seen as necessary for our transition towards higher renewable penetration. For now, they are unable to sell caps through the exchange and will need to take a higher merchant risk or restructure a new product which works better with renewable energy.

This may act as a disincentive for investment in gas fired power stations though AGL is still looking to replace their Torrens A power station with a new gas fired power plant which will be more flexible to respond to change in demand according to AGL. It is hoped that sufficient demand response and batteries can come online in time to firm up the renewable generation. If that is not the case, energy prices will remain elevated for longer.

If you would like to know more about the AEMC and the impacts of this rule change, please contact Edge on (07) 3232 1115 or 1800 334 336.

The Port Augusta located, concentrated solar thermal plant has reached a significant, yet not surprising, milestone in achieving development approval for the plant. The Aurora plant will have 150 MW of capacity and 8 hours of storage.

The development approval suggests that the $110 million concessional loan from the Federal Government is all but secured. It is understood that the funding was allocated in the May 2017 Federal budget and to be administered through ARENA.

The plant is scheduled to deliver 100% of its output to the SA Government under a long term agreement beginning in 2020.

If you would like to know more about renewable energy projects and how they could assist with reducing your energy costs, please contact Edge on (07) 3232 1115 or 1800 334 336.