At the end of September AEMO announced that it was pushing back its draft Marginal Loss Factor (MLF) determination around rule changes put forward by Adani Renewables to November.

Now don’t turn off, Marginal Loss Factors are not the new Dan Brown or Stephen King novel, but they are a hot topic of the NEM at the moment and ultimately will affect the cost of the electricity we all buy. So what are they and why are they important?

What is an Marginal Loss Factor?

Think of a block of flats and you need to fill a bath on the 1st and 10th floors. However, to do that you need to climb up a ladder with a leaky bucket. Each time you fill the bucket and start climbing the ladder you will have more left in the bucket when you reach the bath on the 1st floor than when you reach the bath on the 10th floor. Therefore, to fill the bath on the 10th floor, you are required to use more water (and more trips), compared to filling the bath on the 1st floor.

That is exactly what happens on the Electricity networks (Distribution and Transmission networks). The further away your power generation source be it a thermal station, wind or solar farm, is from where you need to use the electricity i.e. our homes and offices, the larger the losses are (the more water that is needed to fill the bath to the same level)

A MLF is a factor given to each power station which represents how much electricity will be lost between the point it is generated and where it is needed. It is “lost” due to the resistance in the high voltage cables increasing and converting some of this power to heat.

But how does that affect energy consumers? Let’s go back to the bucket for a minute and assume you only need 1 bucket to fill the bath on the first floor but need 10 to fill the bucket on the tenth floor. The company is going to charge you for filling that bucket 10 times (even though it is their leaky bucket and that they only put a tap on the ground floor and not one on the 9th which is causing the problem!) They don’t want to absorb the cost of those losses and affect their profitability, so they pass it through to us. So the bill is more for the person who is on the 10th floor than that of the 1st floor.

It is the same with MLFs, if a station needs to produce twice as much energy to supply a site with electricity due to the MLF, then that cost will be reflected in the sites electricity cost.

AEMO are the calculators of these MLFs and consider the distance from the load centres (Regional Reference Nodes, RRN), the capacity of the current networks, the type of generation (i.e all solar in one area would have relatively similar dispatch patterns) and the new projects coming on in those areas. They then assign each generator their own MLF.

We can’t change physics so why is this news?

So why is this MLF’s a popular topic in the National Electricity Market?

In the past most generation came from large power stations, connected to the transmission network and supplied the main demand “load” centres. This meant that Australia had relatively stable MLF’s and any changes to these factors were negligible. Generators are paid for their bids (to supply the electricity) multiplied by the MLFs, so it affects their cost of generation. Thus, it is important to understand as it affects the costs which are passed through to consumers and for investment decisions for new build generation.

However, we are now in a new world with new types of generation connecting into the network in remote areas and with less predictable dispatch patterns. In many cases these are renewable generation projects which can be built significantly quicker than their thermal counterparts. Reducing the time AEMO have to consider the impact this will have on the network in those areas. This coupled with mothballing of traditional thermal coal units and transmission line constraints has resulted in a significant trend of reduction in the MLFs, which is exacerbated in renewable generation.

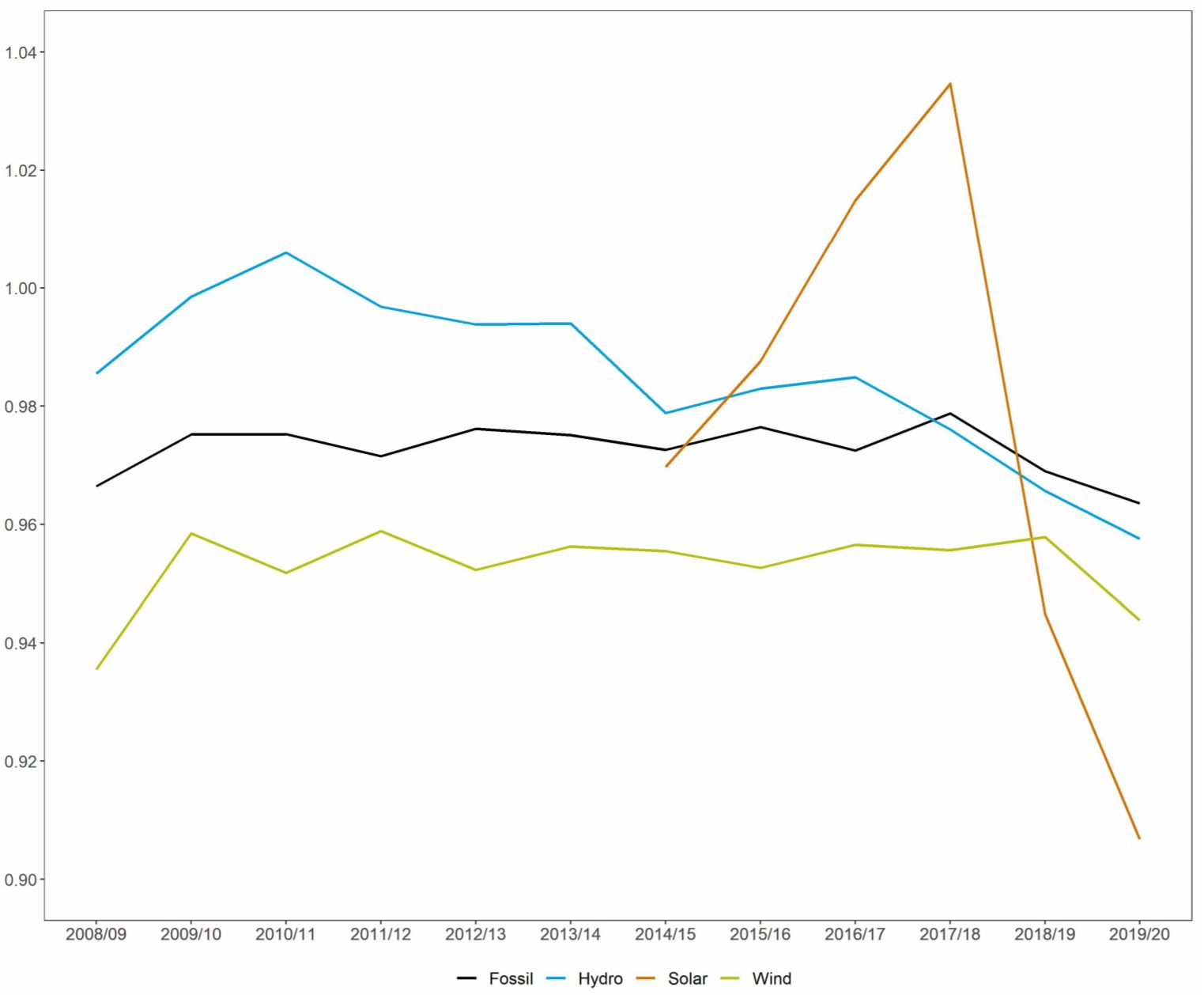

Source AEMC TLF Rule

To try and address the reduction in these MLFs there have been many requests by companies requesting that AEMO change their calculation methodology, with Adani Renewables gaining the most traction in their recent request. Adani Renewables have requested that AEMO change the methodology from a site specific MLF to an average loss factor methodology, basically a regional loss factor for an area regardless of generation type. They argue that it would make the market more competitive and result in lower prices. It would also result in more stable MLFs, giving certainty to investors which will drive investment in existing and new renewable projects due to it creating more financial stability.

How am I impacted?

If this is passed, an average MLF could potentially reduce your bill, either directly due to better competition in the areas with high renewables or through a reduction in Transmission charges. However, this relies on the retailer passing these benefits on.

But if this is not adopted there would be two main impacts to consumers.

The first and most obvious is that with reducing MLFs, the cost of generation in high renewable areas could potentially increase and be passed through to end consumers due to inefficiencies in the market, ultimately leading to higher bills.

The second is a twofold impact and is concerning the cost of LGC’s.

As these are being created through generation in the remote and highly constrained areas of the grid and are linked to their allocated MLF, which are the lowest and fastest reducing MLFs. Less would be generated and therefore available and this could increase their value. The second impact is a longer-term view, in that a reducing and uncertainty in renewable MLFs has the potential to significantly reduce direct investment and development in renewables going forward. With ever increasing requirements for these certificates from industry, end users and retail tariffs the continuance of this pattern could set an upward trend in the price of the certificates.

If you would like to know more about MLF’s and the impact on your cost of electricity, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.