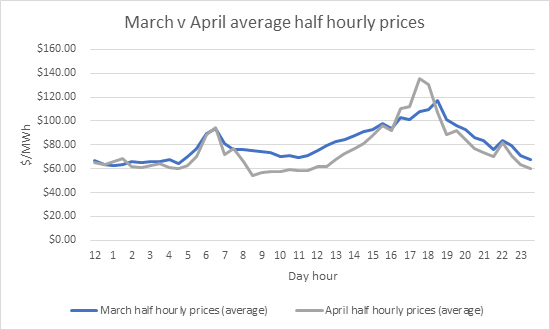

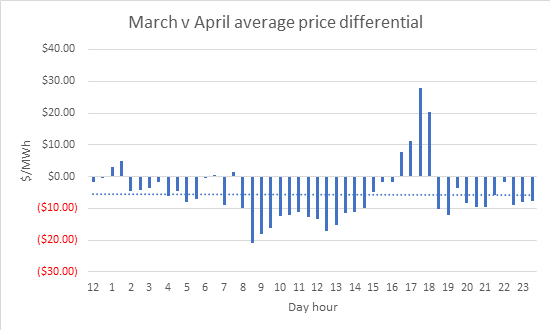

In Queensland, we have observed lower daytime spot prices since the beginning of April, relative to March averages.

Taking a closer look at half hourly average spot prices seen so far in April, we can see that between 8am and 4pm spot prices have been softer than the same periods in March. Following this, spot prices are higher in the evening peak periods. Whilst it is a very small data set, this is the relationship that many in the market expect to evolve.

Softer spot prices in the day will motivate generators to

price more aggressively (price higher) in the evening peak to increase earnings

which have been lost during the day.

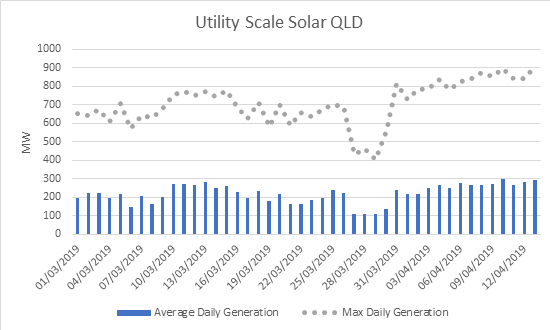

Should we see this evolution of softer spot prices during the sunlight hours of the day, it will put further strain on the Queensland solar industry which has had several setbacks of late.

In addition, we can observe from the below graph that there has been an increase in generation from utility scale solar, in terms of both peak and average generation. The increase in solar is making more low-cost generation available in Queensland. New generation from these solar plants remains insufficient to meet all demand and therefore, solar is not setting prices.

If you have any questions regarding spot prices or any other matter relating to energy, please contact Edge Energy Services on 07 3905 9220 or 1800 334 336.

Established in April 2003, Angel Flight Australia is a charity that coordinates non-emergency flights to assist country people to access specialist medical treatment that would otherwise be unavailable to them because of vast distance and high travel costs.

All flights are free and assist passengers travelling to or from medical facilities almost anywhere in Australia.

Who do they help?

Anyone who is medically and financially disadvantaged, being families who have been financially devastated by medical bills due to illness, accidents or other chronic conditions.

How does Edge support Angel Flight Australia?

For nearly two decades, Alex Driscoll, Manager Wholesale Clients and Markets, has been involved in 4WD adventures to show other participants parts of the country they would not normally be exposed to. Since 2005, Angel Flight Australia has been the recipient of the entry fee paid by each participant. Previous fundraiser adventures have been to Cape York, Simpson Desert, Victorian High Country and Central Australia.

Previous fundraising activities include the Stoney Creek Mini Music muster run over a weekend with music, food and activities, with all proceeds going to Angel Flight Australia.

What is the best piece of advice you have ever received?

Your title isn’t only what you put on your business card; it is what you do with your position that counts.

Name a place you have never been to and would like to visit. Why?

Everest. It’s the highest place on earth so would be an amazing achievement to stand on the top.

Who or what inspires you?

Self-made successful people inspire me, being the likes of Richard Branson, Sid Kidman and Ranulph Fiennes. These people generally take risks to challenge themselves or create any opportunities.

What is one of the biggest challenges facing energy customers today?

The energy market is constantly changing with new technologies, pressure put on the network resulting from the changing energy mix and policy makers struggling to keep up with these changes. As a result, customers are challenged to make energy decisions with such a high level of change and uncertainty. Adding to this, new concepts are constantly entering the energy discussion and consumers are struggling to gain the knowledge to understand the topic and how it impacts them.

What does a typical day look like for you at Edge?

No day at Edge is ever the same for me. One moment I will be contract trading, the next moment I am modelling the forward curve, working on a new project or on the phone providing advice to clients.

Alex Driscoll, Manager Wholesale Clients and Markets

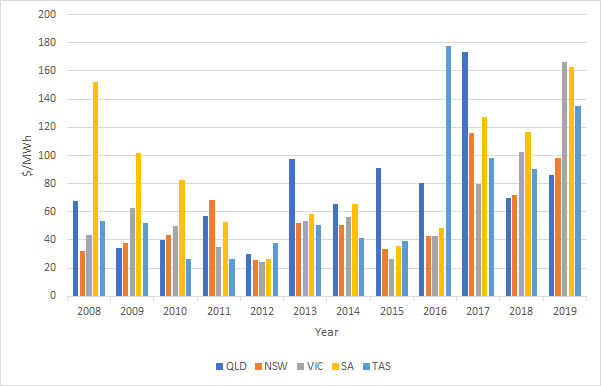

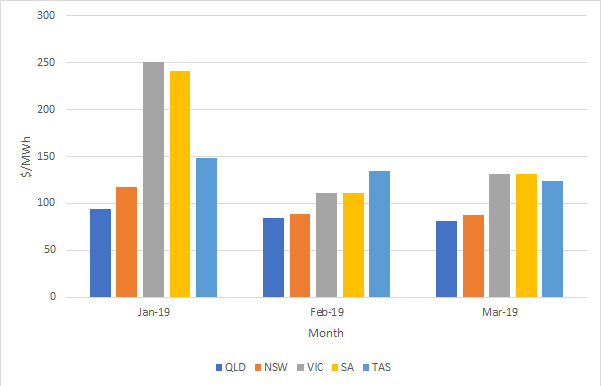

The electricity spot prices were higher for the Summer period (January – March) compared to the preceding three months. Although demand remained static, prices increased as a result of coal and gas generation setting prices at elevated levels. Average prices increased in all regions from the previous summer, with Queensland increasing the least at 23% and Victoria increasing the most at 62%.

Across all regions, prices during the 2019 summer were higher than the 2018 summer and were very high in a historical context for Victoria, South Australia and Tasmania. Looking back across the last 10 summers, 2019 summer prices are at their highest levels in most states.

Figure 1: Historical prices for summer

It should be noted that prices in both 2012 and 2013 were affected by a carbon tax, which was subsequently repealed in 2014. Since then, there has been a steady price increase in all mainland NEM regions. In Queensland, the Government provided a direction to Stanwell Corporation and CS Energy to adopt strategies to reduce wholesale prices. Since the direction, there have been fewer price spikes (prices above $300/MWh), although average prices have continued to increase.

Price spikes in late January for NSW, South Australia and Victoria were driven by a combination of the following factors:

the lack of wind generation;

reduced limits on interconnectors;

reduced thermal generation output; and

hot weather increasing demand.

High temperatures also increased demand for Queensland in mid-February, pushing demand to 9,988MW.

The New South Wales market was relatively stable over summer with limited volatility. Throughout the season, prices only spiked above $500/MWh for the trading interval on 2 occasions. Snowy Hydro continues to draw down its dam levels to cover cap contracts and supress prices below $300/MWh.

Quarter 1 2019 saw a lower level of generation for gas powered generators as a result of the increased level of generation from renewables and the rising cost of fuel. Renewable generation continues to grow to over 3GW from the start of the year. Operational demand dropped to its lowest level since 2002 as a result of a reduction in energy intensive industries and the increased uptake in rooftop solar PV.

Figure 2: Average monthly spot prices in the NEM

Coal fired generation was at its lowest level since the start of the market on 13 December 1998. This lower level of generation was driven by prolonged outages at Yallourn and Loy Yang A and the increase in market share from renewables. Coal fired generation was also impacted by an increased number of trips, increasing from 10 in the previous quarter to close to 30 in Q119.

Hydro generation was reduced driven by lower dam levels or water conservation strategies by Snowy Hydro in New South Wales and Victoria, and Hydro Tasmania in Tasmania.

Looking forward

Higher spot prices and concerns over the stability of the grid have caused the forward curve to increase. Snowy Hydro continue to draw down on its dam reserves and with a dry outlook, the inflows could be lower than previous years. If Snowy Hydro reduce output during 2019, spot prices could be even higher than current prices.

There is currently a huge pipeline of committed projects waiting to enter the market. These projects are mainly renewable energy, diesel and batteries. The integration of renewable energy generation into the market and the strategies of price setting coal and gas generation will determine if prices will reduce or if a more volatile market will be created. It is unlikely in the near term that spot prices will return to historical levels as renewable generation has not reached the volume required to consistently set prices at lower levels.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Manager Wholesale Clients and Markets, Alex Driscoll on 07 3905 9220.

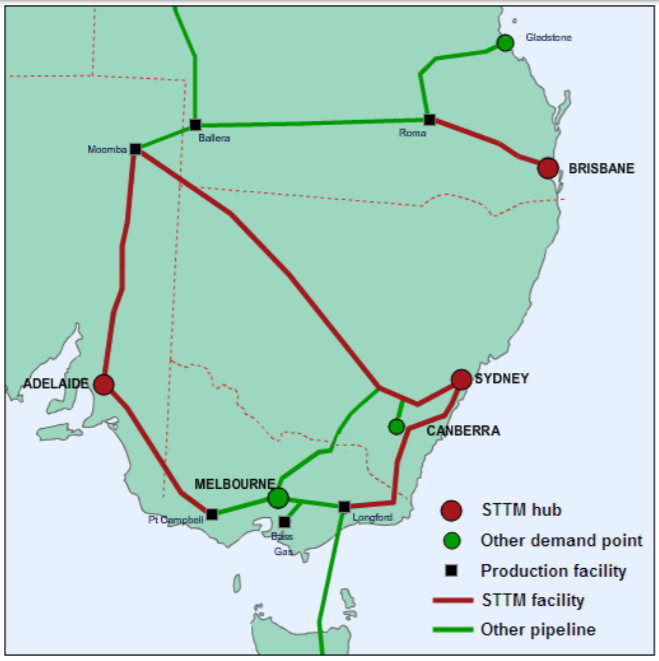

For a growing number of large energy consumers, consideration is turning to whether entering standard vanilla retail gas agreements deliver the most effective outcome. For consumers who are located within the bounds of the Sydney, Brisbane or Adelaide Short Term Trading Market (STTM) markets, many may not be aware that there is an alternative way to purchase gas. Below, we consider how the STTM works and what the benefits are of exploring this option.

What is the STTM

The STTM is essentially a market for the trading of natural gas at a wholesale level at defined hubs between pipelines and distribution systems. The STTM is a day-ahead gas market operated by the Australian Energy Market Operator (AEMO) with hubs located in Sydney, Adelaide and Brisbane. This means that gas is traded a day ahead of the actual gas day. The market settles daily with “shippers” delivering gas and “users” consuming gas. An organisation may sell gas as a shipper and purchase gas as a user through the same STTM, however, it would do so at the daily market price.

Source: “Overview of the STTM for Natural Gas”, AEMO, page 1

Market participants are incentivised to ship and consume volumes of gas nominated through a pricing mechanism, which aims to keep the gas supply system balanced. Organisations are able to sell excess gas to its requirements on the open market the next day, as well as bid to purchase extra gas as and when required. This system allows participants more flexibility and choice in purchasing gas supplies. Furthermore, the STTM’s price transparency ensures that the price set by the market daily truly reflects the current supply and demand situation.

Each of the STTM hub settles independently of the other, however each hub operates under the same rules outlined by AEMO.

There are a range of drivers for some large gas consumers transitioning to purchasing and selling gas in the STTM. The main reasons are:

The STTM is an historically lower commodity cost;

Consumers can manage or avoid penalties under daily, monthly, and / or annual take or pay positions;

There is increased flexibility for both sellers and consumers; and

There are no long-term commitments.

These benefits can materially lower the cost of consuming gas. Depending on the nature of the organisation, there are a range of structures to access an STTM. Each structure requires varying levels of engagement from the consumer.

Engagement with Edge

To assist in transitioning your organisation to accessing the STTM, Edge are able to offer the following services:

Daily nominations and trading;

Monthly reconciliation;

Facilitation of short and long-term Gas Supply Agreements; and

Managing the STTM application.

Entering the STTM market is strategic decision for most organisations and can take anywhere between 3-12 months to transition. If you would like to know more, please contact us to understand if accessing the STTM market is the right decision for your organisation.

We note that there are also alternatives for consumers who are not within the STTM limits, however these options are not discussed for the purposes of this article. If you would like further information on your options, please contact your Manager Wholesale Clients or Edge on (07) 3905 9220.

As of 1 March, the new Capacity Trading Platform (CTP) and Day Ahead Auction (DAA) came online. This market arose after the Council of Australian Governments (COAG) Energy Council agreed to implement the legal and regulatory framework required to give effect to the capacity trading reform package, as recommended by the Australian Energy Market Commission (AEMC) as part of its Easter Australian Wholesale Gas Market and Pipelines Framework Review.

The reforms apply to the operators of transmission pipelines and compression facilities operating under the contract carriage model (collectively referred to as “transportation services”). The objective of the reforms is to encourage and facilitate trading of unutilised capacity on non-exempt transportation facilities. This is achieved by providing shippers with an incentive to trade spare capacity on a secondary capacity market (the CTP). If a shipper fails to sell any spare capacity prior to the nomination cut-off time, then its contracted but unnominated (CBU) capacity is then offered to other participants in an auction conducted a day ahead of the gas day (the DAA). In contrast to trades conducted by shippers prior to nomination cut-off time, the proceeds from the auction are retained by the service provider, which incentivises shippers to sell their spare capacity ahead of nomination cut-off time. (AEMO, Pipeline Capacity Trading: Overview, 2018).

According to the Australian Energy Regulator (AER) in the first two weeks of the DAA, 1.87 PJ of capacity was bought across multiple pipelines and compressors (Australian Energy Regulator, Gas Market Report, March 2019).

C&I Gas pricing

C&I gas contracts continues to be an opaque market. Contract prices have softened since the peak in 2016, however remain high and continue to put businesses under strain who are challenged with either absorbing higher costs or passing these onto customers.

AEMO recently released their Gas Statement Of Opportunity which reinforced the situation that domestic gas supply and demand balance is tight. AEMO highlighted that:

“Supply from existing and committed gas developments is forecast to provide adequate supply to meet gas demands until 2023. However, risks remain that any weather-driven variances in consumption or electricity market activity could increase gas demand, creating potential peak-day shortages as outlined in AEMO’s 2019 Victorian Gas Planning Report”.

Weather driven variances in consumption were observed in late January this year when the Cumulative Price Threshold was met and the Administered Price was activated VIC and SA. This highlight from AEMO is generally concerning as it suggests that there is unlikely to be any reprieve in gas prices in the near to medium term.

Recently, pricing for C&I customers has been observed between $11.00/GJ and $14.00/GJ subject to terms and conditions. Customers are increasingly looking at taking on more responsibility for their consumption in an effort to bring down the commodity price.

Gas Powered Generation

Gas powered generation in Q119 was 4% higher than Q118 with less generation from hydro, black coal and brown coal. There was a material increase in generation from solar and wind resources which was to be expected.

Average prices in the STTM hubs and the VIC gas market all increased in Q119 relative to Q118. Volumes were lower in the STTM markets, whereas the volumes increased through the VIC market. Gas fired generation in VIC averaged 75TJ/day in Q119, which was 23TJ/day higher than Q118. Less generation from brown coal and hydro generators was the primary driver behind this.

Regional analysis

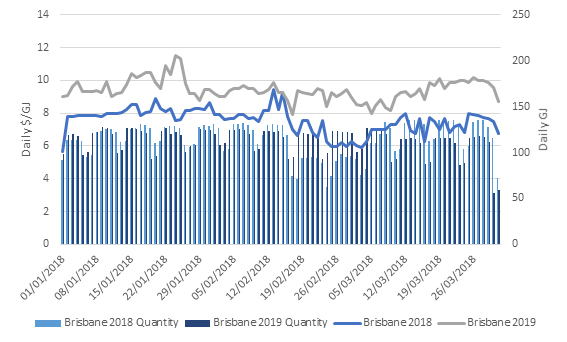

Brisbane

Brisbane STTM gas prices were higher in Q119 relative to Q118. Prices were consistently higher and generally followed a similar pricing trend. Volumes exchanged through the STTM were marginally higher in Q118 relative to Q119.

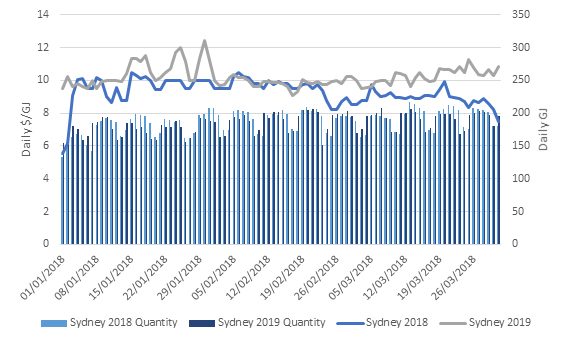

Sydney

Sydney STTM gas prices were higher in Q119 relative to Q118 with a divergence in prices in the final week of the month. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

Adelaide

Adelaide STTM gas prices were higher in Q119 relative to Q118. Q119 prices were consistently above that of Q118, with the exception of a few days at the beginning of February. Volumes exchanged through the STTM were very marginally higher in Q118 relative to Q119.

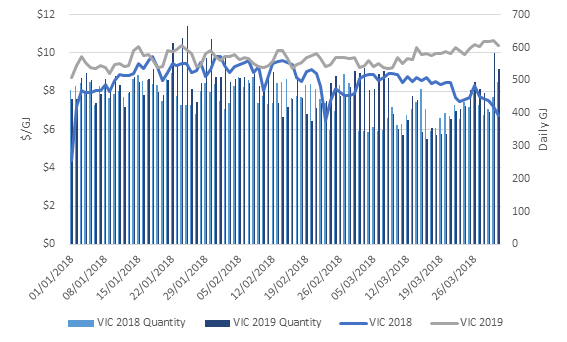

Victoria

VIC gas prices were higher in Q119 relative to Q118 with prices diverging in the final weeks of the quarter. Unlike the STTM markets, there was more volume traded through the VIC market in Q119 relative to that of Q118. On the 24th and 25th of January, there was a spike in gas volumes which was driven by higher demand from the Gas Powered Generators as a result of very high electricity prices.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220.