RCR Tomlinson entering voluntary administration this week has been a major eye-opener in the renewable energy world. The engineering firm had shown signs of stress earlier in the year, particularly when it was forced to record a $57 million write-down on the value of it’s Daydream and Hayman solar farms in Queensland. Following this, the company successfully went to market and raised an additional $100 million in capital. Now after incurring liquidated damages as a result of running late on solar projects, directors had no choice but to put the company into administration.

In the renewable energy space, these events particularly emphasise the potential risk of entering into a PPA with a project that requires development prior to receiving any MWh. For those considering entering into a renewable PPA, it is imperative to be mindful of the gravity of the project risk taken with these developments. With increasingly stringent connection criteria being enforced by AEMO and transmission companies, corporate PPA off-takers need to consider the structuring of risk in the PPA to avoid being exposed in situations like this.

There are several ways to manage project risk through legal and commercial arrangements. Without being privy to the details of RCR Tomlinson’s contracts, it would appear that the company was wearing “connection to the grid” risk. On face value, this would have felt like a win to the off-taker. However, the off-takers are now in a position where the risk has fallen onto them due the collapse of the company. Whilst RCR Tomlinson shouldn’t have taken that risk, the PPA counterparties arguably also should not have turned a blind eye to the potential project risk.

This is an important lesson for any corporate entity looking to enter into a PPA, by understanding whether your developer and construction partners have the appropriate means to manage the risk that is placed on them. Having liquidated damages in a contract is essential. However, be mindful that at the end of the day, if a company is placed into administration and subsequently liquidated, liquidated damages are worthless.

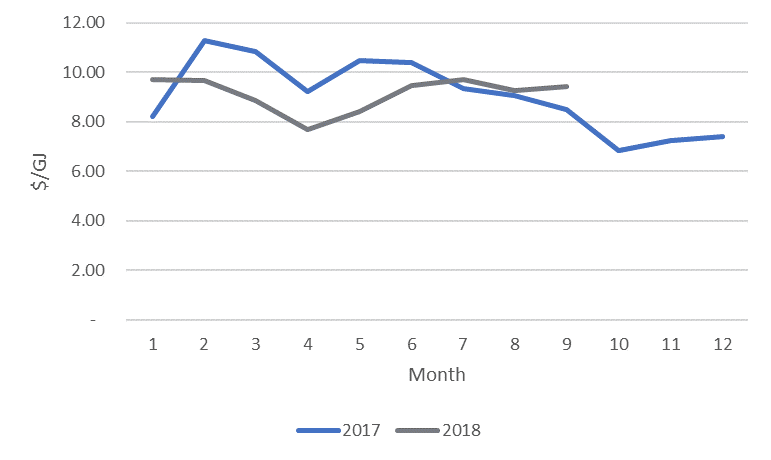

The electricity spot prices were generally higher for the winter period (June to August) than the preceding three months. The largest contributing factors were higher gas prices and increased demand for most of the regions. This excludes Tasmania where average prices fell from $80.26/MWh in autumn to $47.55/MWh in winter. Demand was still higher in the Tasmanian region, however additional rain meant that many of the hydro plants were running, as opposed to spilling water without generating. This put downwards pressure on the local prices.

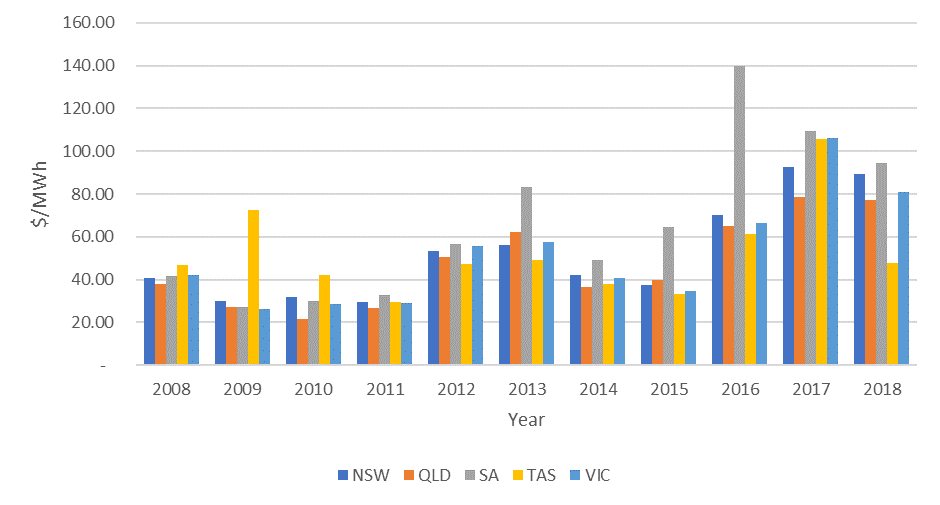

The lower Tasmanian prices didn’t result in lower prices for the rest of the National Electricity Market (NEM). Across all regions, the prices during the 2018 winter were lower than the 2017 winter, however were still very high in a historical context. Looking back across the last 10 winters, the previous two (three for South Australia where Northern Power Station closed in May 2016) look like outliers. In fact, averaging the previous 8 years from 2008 to 2016, prices have been lower for all regions.

Figure 1: Historical prices for winter

It should be noted that prices in both 2012 and 2013 were affected by a carbon tax, which was subsequently repealed in 2014. Since then, there has been a steady price increase in all mainland NEM regions. The prices appear to have plateaued, however not reduced. In Queensland, the Government provided a direction to Stanwell Corporation to adopt strategies to reduce wholesale prices. Since the direction, there have been fewer price spikes (prices above $300/MWh). Although, the prices outside summer months are not reducing. Queensland is the only NEM region which had lower demand during winter compared to autumn. Price spikes in June caused by issues on the transmission network and lower availability at the start of winter kept average prices higher.

New South Wales had the same transmission issues as Queensland, and rolling planned outages at coal fired power stations meant that there was little spare base load capacity available. Victoria had high overall prices with few price spikes and was the only NEM region which didn’t have any prices above $350/MWh. Higher demand and gas prices kept overall prices high in the region. With lower availability in New South Wales, Victoria exported an average of 389 MW into the region compared to 57 MW during autumn. South Australia is heavily dependent on gas powered generation when there is insufficient renewable generation to power the state. This makes South Australia vulnerable to higher demand and higher gas prices, both of which were prevalent during winter. Prices were the lowest in three years, however still the highest of any NEM region. There is still a large amount of domestic gas usage in South Australia which means that prices tend to spike during winter. This occurred again in 2018.

The market didn’t run completely smoothly during the winter period. On Saturday 25 August 2018, multiple simultaneous lightning strikes on critical infrastructure caused load shedding. The lightning strikes occurred on the border between New South Wales and Queensland causing a loss of the main interconnector between these two regions. At the time, Queensland was supplying New South Wales with generation. The sudden loss of generation from Queensland caused load to be tripped in New South Wales. The loss of frequency also triggered a shutdown of the interconnection between South Australia and Victoria for reasons still being investigated by AEMO. This caused load shedding in Victoria and Tasmania. In total, 800 MW of load was lost in New South Wales, 280 MW in Victoria and 80 MW in Tasmania. This was predominantly industrial load which was reconnected within an hour.

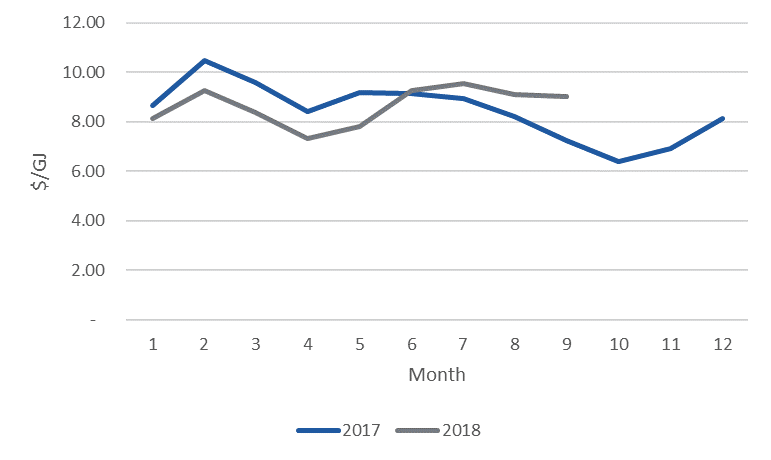

Higher spot prices and concerns over the stability of the grid has caused the forward prices to increase. Snowy Hydro continued to draw down on its dam levels and with a dry outlook, the inflows could be lower than previous years. If Snowy Hydro reduces their output during 2019, spot prices could be even higher than current prices.

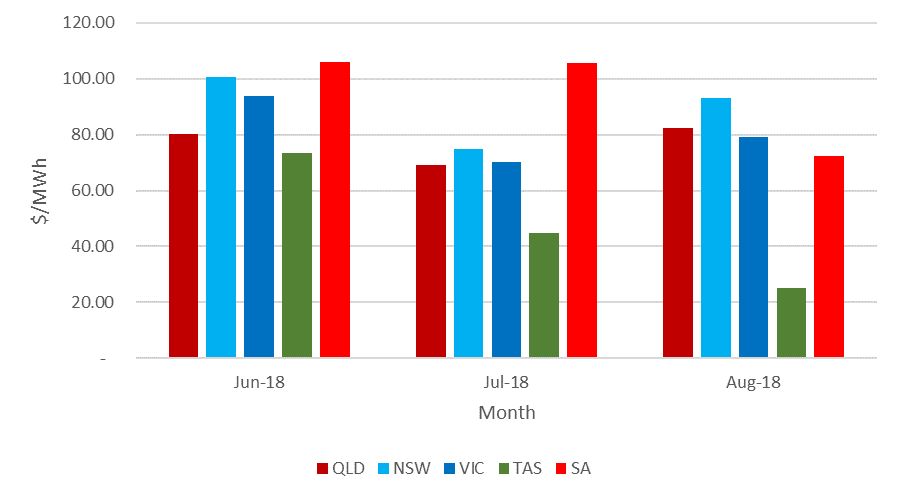

We are also seeing a separation between prices again. Though there were increases across all states, these were highest in Victoria ($16.56/MWh) and New South Wales ($15.88/MWh), and lowest in Queensland ($7.38/MWh).

Figure 3: Calendar year 2019 forward contracts

NSW

QLD

SA

VIC

01-Jun-18

68.18

62.53

87.00

74.00

31-Aug-18

84.06

69.91

96.09

90.56

Source: ASX

There continues to be additional generation added to the market, mainly renewable energy. Going forward, it will be the integration of this renewable energy into the market which will ultimately determine if prices will reduce or if a more volatile market will be created. It is certainly unlikely in the near term that spot prices will return to historical levels (where the cost of energy during winter was in the $30s/MWh).

Looking forward

Q119 continues to be a period of concern across the market, as market participants continue to accept higher prices for swaps in the interest of reducing or removing exposure to spot prices. The BOM is forecasting hot and dry temperatures during the period, which are conditions that tend to cause volatile and higher spot prices.

If you would like to discuss the electricity market outlook and potential impact to your electricity portfolio, please contact our Energy Analyst, Nick Clark on 07 3905 9227 or on 1800 EDGE ENERGY.

In late 2017, the Energy Security Board (ESB) developed a scheme to provide investment certainty in the electricity market, which would address Australia’s commitments under the Paris Agreement.

The Coalition had ruled out a carbon tax, other cap-and-trade schemes and virtually any other scheme which had been attempted in the past. This left very few options for the ESB to appropriately address investment certainty in the electricity market. The ESB eventually developed an innovative scheme called the National Energy Guarantee (NEG). The basis of the NEG was essentially a cap-and-trade scheme for environmental certificates and, as a sweetener, it also had a reliability obligation. Essentially, the scheme was linked to contracts with retailers to make it sound like it wasn’t a cap-and-trade scheme. The reliability obligation would force retailers to purchase firm contracts if there was a reliability gap. The additional demand for firm contracts was thought to increase demand for firm generation.

The Australian Labor Party (ALP) was willing to support the NEG on the assumption that they would be able to increase the target for carbon reduction. The states were also largely on-board, on the basis that state-based schemes could continue under the NEG.

The new focus of the Federal Government will be reducing prices in the energy sector.

Prior to the legislation being enacted, Malcolm Turnbull was removed as Prime Minister. Even though Scott Morrison, the succeeding Prime Minister of Australia, had previously been supportive of the NEG, he conceded that it would no longer be acceptable to his party and declared the NEG dead. At the same time, the Australian Competition and Consumer Commission delivered a paper suggesting ways of reducing electricity prices. The new Energy Minister, Angus Taylor, was nicknamed the “Minister for Bringing Prices Down” declaring the new focus for the Federal Government in the energy sector.

Subsequently, the ALP has been quietly arguing for bipartisan support to potentially revisit the NEG in its entirety. Recently, Mr Morrison has been open to the reliability portion of the NEG being resurrected. Mr Morrison has expressed interest in meeting with the states and territories to discuss the possibility of legislating the reliability aspect of the NEG on its own.

While the NEG is still a topic of conversation in parliament, it seems that only the reliability obligation may survive.

As a whole, energy policy is shaping up to be a key differential in the next Federal election. In the meantime, we are seeing renewable projects going ahead across the entire system. Australia is well on track to meet and exceed the current 2020 target of 33,000 GWh of renewable energy across Australia. New investors in Australia are coming to terms with political instability, instead focusing on setting projects up directly with businesses that are considering their own schemes due to the lack of political leadership shown in Parliament.

As we come towards the end of 2018, the outlook is grim for bipartisan support of long-term energy policy; however, we may still have a way forward as consumers start to forge ahead of the political vacuum. The Federal government has warned against businesses forming a technocracy to effectively create laws, however given the failure of the government to provide an alternative, this may be the way that policies will be formed going forward.

Domestic gas prices have increased again as Queensland continues to export most domestic gas overseas in the form of Liquefied Natural Gas (LNG). Outages in early 2018 had limited output from the LNG facilities, however all trains are now available.

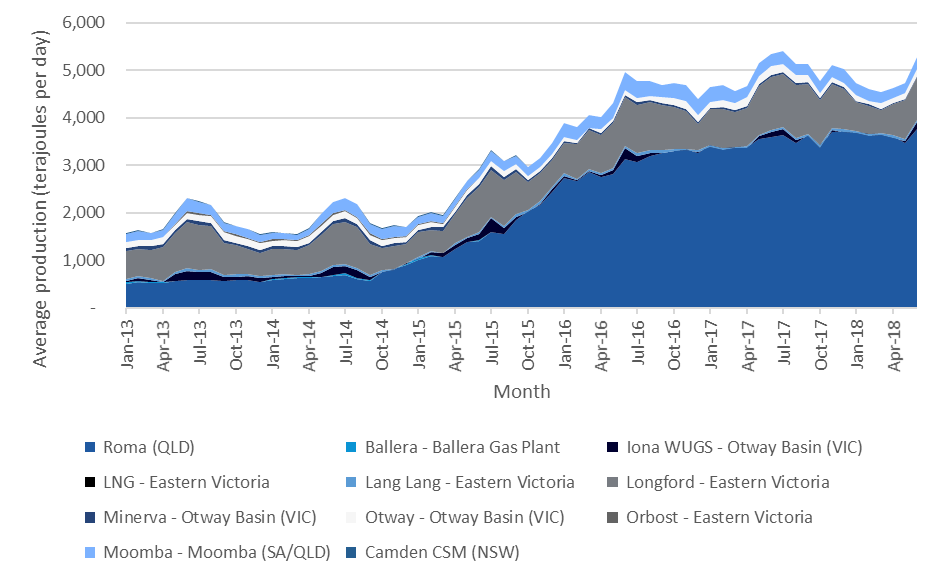

The increase in total gas extracted on the East Coast of Australia is the largest contributor to the increase in gas prices. Before LNG demand, domestic gas could be extracted from cheap resources. However, as more gas is extracted from Roma, Queensland, the price of extraction has increased, which is then passed onto consumers. With the ability to sell gas overseas, producers are also looking to obtain a similar price domestically when the cost of transport has been taken into account (so called netback prices).

The Australian Energy Regulator (AER) has published the average daily production of gas by production point. This shows the large increase, particularly for Roma. The volume is necessary to justify the very high fixed costs of liquefying and exporting gas.

Source: AER

Overall, prices were lower at the start of 2018 and the Federal Government has been quick to point to its domestic gas policy, whereby producers could be forced to sell gas to domestic consumers ahead of exporting it in the event of a shortage. The inference is that without the domestic gas policy, prices would have been higher. A more obvious driver would be lower export of LNG as one of the export facilities was undergoing planned maintenance. With all facilities now back online, the prices have crept back up and are now higher than the same period in 2017 for all regions.

The Australian Labor Party (ALP) announced that it would look to further strengthen the domestic gas policy by forcing producers to sell locally before exporting if prices were too high. This goes beyond the current policy which requires a shortage for the gas policy to apply. The ALP has not indicated what they consider to be “high prices” for the policy to apply. Additionally, producers are concerned about uncertainty at a time when the gas market needs further investment. The current state of the electricity market should serve as a warning of what happens when there is little investment certainty.

Regional analysis

There are regional differences in the gas prices, which are mainly based on the different usage of gas. In Queensland, gas is mainly used for LNG export while in Victoria it is predominantly used by residential and commercial customers, particularly for heating. In South Australia and Tasmania, gas is still mainly used for gas powered generation (GPG).

Gas usage in 2017 by sector and region

Residential / commercial

Industrial

GPG

LNG

Regional gas consumption (PJ)

Queensland

<1%

8%

3%

89%

1,377

New South Wales

37%

42%

21%

0%

130

South Australia

11%

23%

66%

0%

101

Tasmania

5%

33%

62%

0%

15

Victoria

55%

30%

15%

0%

228

Total

10%

14%

10%

66%

1,851

Source: AEMO

Queensland

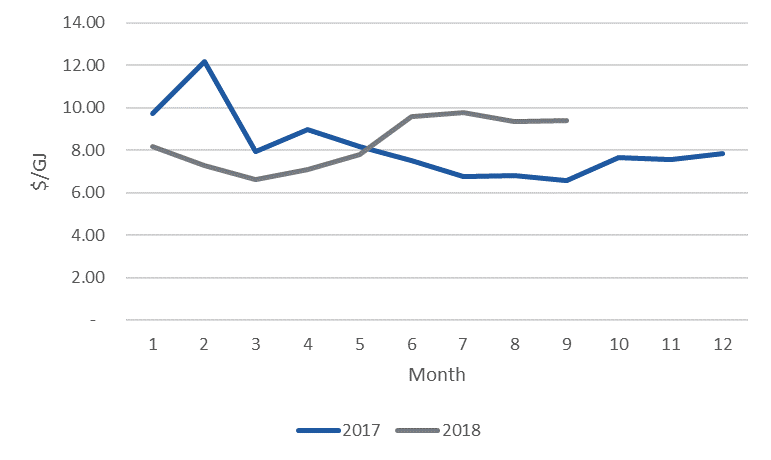

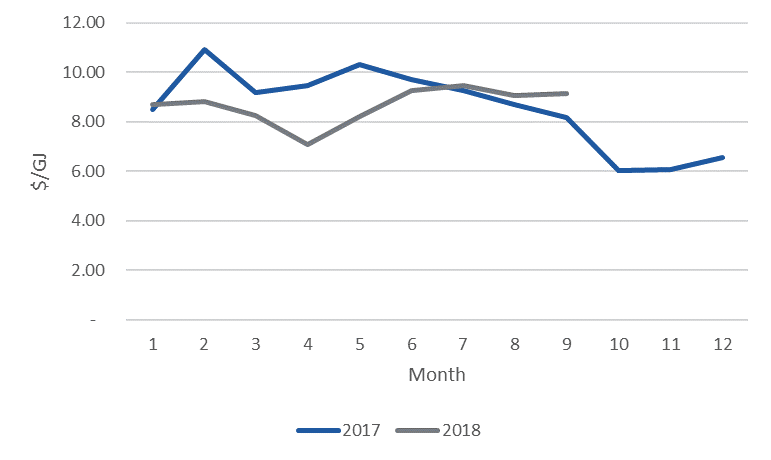

With lower exports in early 2018, gas prices at the Brisbane hub have been lower than the previous year. Once the outage at an LNG facility was completed in June, prices went back to their elevated levels and have subsequently been sitting above the 2017 prices. In the short term, there is limited opportunity for production of gas to stop, which means that shut downs of facilities will tend to lower prices.

Since the increased LNG production, prices in Queensland have remained steady, consistent with prices in 2017 before the shutdown. There is little gas used outside of LNG in Queensland, therefore making it the main driver.

New South Wales

Gas is primarily used in industrial process in New South Wales, providing a flat demand across the year.

From the above graph, it is apparent that prices have been stable across most months. There were slightly lower prices until approximately June 2018 as cheaper gas flowed from Queensland. Prices have started trending up since then.

South Australia

Gas in South Australia is predominately used by gas powered generators. These tend to operate more in both summer and winter when demand for electricity is generally higher.

South Australian gas prices have been modest throughout the year. Higher demand for gas generation in February increased prices overall, however the largest change was again in June when the Queensland LNG facility started exporting again after its outage.

There is still a large swing component of gas demand in South Australia due to residential/commercial demand. Even though this only represents 11% of overall consumption it tends to be very concentrated for a few days per year.

Tasmania / Victoria

There is no separate Tasmanian gas market with most contracts based on the Victorian prices.

Victoria also has the largest proportion of gas being used by residential/commercial consumers. This creates a large swing in gas demand throughout the day and throughout seasons. Unlike South Australia which uses a lot of gas for power generation, Victoria mainly relies on coal. This means that prices are typically lower in summer and higher in winter.

If you would like to know more about what is happening in the gas market and how your business may be affected, please call Edge on 07 3905 9220 or contact your Edge Portfolio Manager.

After celebrating ten years in business last year, 2018 has been a year of reflection. As founder and Managing Director, I especially have been reflecting heavily on why the business started, how it has become what it is today and, perhaps most importantly, where the business is headed.

One thing I’m very proud of is that the ethos of Edge has been unwavering since inception. Edge was established to deliver value. At the core of every decision we make and everything we do is ensuring large energy users are equipped to achieve superior energy outcomes. Put simply, we do everything possible to provide the tools and means to buy better.

They say you are only as good as your team. If I reflect on that, Edge’s performance is a reflection on the evolution of the team over the past ten years. Attracting and retaining suitable staff is so important in any business. In the energy industry, it is critical. Knowledge, experience and industry-based networks add immense value to the capabilities of our team, and ultimately the outcomes for energy users that entrust us with their portfolios. As a relatively small player in an elite league, we punch above our weight to attract the talent that do justice to our ethos and the portfolios we manage. We do this through a client base that exceeds any other in the market, and by having established a reputation for the core values we adhere. Integrity, honesty, trust, loyalty and respect are so much more than words in a policy document. They are at the heart of everything we do.

The reason for this business is still as relevant as the day it was established. We deliver value, and more than ever we love doing it. We’ve been successful in building a portfolio of top tier clients and establishing ourselves as a respected counterparty amongst the largest of players in our industry. We work closely with the largest retailers, generators, and law firms across the market. And we work directly for some of the largest and most trusted consulting names in the world. Despite all of this, there is no denying that many consumers don’t even know our name. And we want this to change.

Edge’s services have reached under fifty of the largest names in our market, with approximately 7.5TWh currently under management and over 10TWh contracted in 2018. Our gas portfolio is small in comparison. Looking forward, first and foremost we want to enhance the way we manage this portfolio. Restructuring the team has been a major focus, with a move to offer each client an even deeper pool of skills and experience dedicated to their portfolio. Portfolio Managers who were once tasked with delivering many aspects of a client’s requirements have recently been phased out of the business. Replaced with more senior dedicated managers of wholesale clients for strategic management and dedicated account managers for more transactional services. Each Manager Wholesale Clients will ultimately ensure that their portfolio is being optimised. They’ll be heavily supported by their dedicated Account Manager, our Markets and Advisory team, and our IT team through The Edge Energy Management System (TEEMS) and our customer facing portal (Edge LIVE).

We want to reach more portfolios, and exponentially increase the clients we represent. We want all business energy users in Australia, not just the top tier, to know our name and the immense value our team will bring to their portfolio. Commencing in early 2019 we will invest in dedicated sales personnel to market our services throughout the market. A dedicated BDM will target consumers more suitable for Edge Energy Services’ portfolio, whilst a Channel Manager will be positioned to focus on stand-alone Edge LIVE (BI platform) and Edge Utilities (SME brokerage) services.

Briefly and in closing, our service offering has exploded in recent years, with the development of in-house spot forecasting models, brokerage services on environmental and renewable transactions, and specialist advisory services around FCAS, embedded generation, and generation revenue optimisation strategies. We look forward to outlining these further in the next edition of Edge Insights.

In the meantime, we warmly welcome all feedback on the recent changes to the team and ultimately the management of your portfolio. This feedback is essential to us ensuring you are getting the value we constantly strive for.

What is the best piece of advice you have ever received?

Failure is the best teacher there is and it provides an opportunity to learn and better yourself. You cannot grow without failure.

Name a place you have never been to and would like to visit. Why?

I would love to do the Overland Track in Tasmania. It has been on my bucket list for some time now. I was born in Tasmania, so it holds a special place in my heart. The wilderness is also spectacular in Tasmania. My ideal holiday would be spent camping and hiking through the wilderness. There is nothing more refreshing than getting out in nature, challenging yourself and getting away from civilisation.

Who or what inspires you?

Without sounding cliché, my grandmother is my inspiration. She grew up in a small, 1 room, stone cottage in Ireland with very little. She was a mid-wife in the war and didn’t have an easy life. She was a very hard worker and an extremely resilient person. Despite her hardships, she was very caring and gentle (everyone loved her), she always had a very positive outlook on life and (although unintended) she always ended up the life of the party. I aspire to be like her every day.

What is one of the biggest challenges facing energy customers today?

Managing the integration of increasing renewable generation into the existing grid. This challenge is diverse and filters into issues around reliability, affordability and political debate. An increase in the investment of renewable generation is a positive thing, but it does pose challenges of solving for intermittent generation and increasing bidirectional electricity flows.

When there are reduced sources of wind or solar, the question becomes how we ensure a reliable source of energy to guarantee supply will match demand in real-time. This has sparked growth in how energy storage and battery can help. Due to increasing amounts of residential Solar PV installation, energy flows are increasingly being sent back into the grid rather than drawing from it, creating the challenge of how to manage the distribution network effectively and securely.

What does a typical day look like for you at Edge?

I usually arrive between 8am and 8:30am and take a moment to plan out my day. Part of my role is to support Stacey as Managing Director. I will check Stacey’s calendar and compile a to-do list for both of us. Each morning, I join the Markets & Advisory team to discuss what is happening in the energy markets. In addition to having recurring monthly and weekly tasks, such as accruals and invoice reconciliations, I also track progress of projects for clients, organise meetings with clients, follow up on any client enquiries, and provide administrative support to the Edge team. The energy sector is complex and there is a lot to learn, but I am so thankful to be part of such an interesting industry and work alongside such a talented and knowledgeable team.

As 2018 continues to fly by, Christmas is now right around the corner. At Edge, we recognise that the reality of Christmas is very different for many families in our community. Christmas isn’t always a time of celebration, family, friends and gift giving.

In lieu of providing Christmas cards to our customers each year, Edge donates to a local charity to help support members of the community who struggle through the Christmas season. This year, Edge will be donating to Foodbank Queensland.

Foodbank is the largest hunger relief organisation in Australia, providing enough food for over 67 million meals last year alone. The aim of Foodbank is to combat food insecurity, which affects 15% of the Australian population. Foodbank works with the entire Australian food and grocery industry including farmers, wholesalers and retailers to provide food to those in need. Throughout the Christmas period, Foodbank creates Christmas hampers to give everyone an opportunity to celebrate and enjoy time with family and friends.

Together with Foodbank we can all make a difference this Christmas. Aside from monetary donations, Foodbank welcomes donations of food and services, including assistance with packing Christmas hampers in the lead up to Christmas Day. For more information and to provide a donation, visit http://foodbank.org.au.