Melitta has spent over a decade working in the energy sector in roles including Retail Pricing Analyst, Account Manager and Customer Relationship Manager. As Portfolio Manager at Edge, she focuses on building and maintaining strong relationships with clients and key stakeholders. She’s unwavering in her commitment to using the Edge’s efficiencies and insights to deliver solutions that save clients time and money.

What is the best piece of advice you have ever received?

It’s not necessarily advice, but a quote from Winston Churchill has stuck with me over the years. “Continuous effort – not strength or intelligence – is the key to unlocking our potential”.

It is the little things that we do each day that add up to big changes.

Name a place you have never been to and would like to visit. Why?

I would really love to travel through South America. The culture, the food and the history all entice me to travel there. Highlights would certainly be trekking through the Amazon and seeing Machu Picchu.

Who or What inspires you?

Communities and social enterprises that are working for the improvement of the environment and society inspire me. I have made many changes in my life that impact both myself and my daughter and I hope to encourage others to make changes by having conversations and sharing my personal experiences. If we all could make one positive change towards the environment every day, imagine the global impact. The actions of individuals can have far-reaching effects.

What is one of the biggest challenges facing energy customers today?

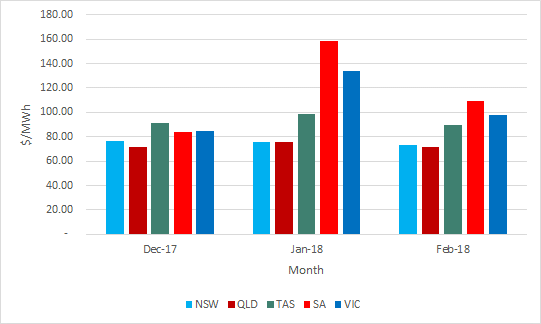

In such a volatile energy market, reducing energy costs is a serious challenge for businesses. With pricing in both the gas and electricity markets doubling in recent years, costs that would have generally been low percentage OPEX are now being highlighted by management as critical areas to review.

Energy efficiencies, renewables, Power Purchase Agreements and on-site generation (including solar PV and battery storage) all tend to be at the forefront of conversations with clients and prospective clients as they try to navigate the best path forward for reducing energy costs for their businesses.

What does a typical day look like for you at Edge?

On any given day I will have a number of scheduled client deliverables which could include weekly and monthly market reporting, site specific accruals and reconciliation reporting. Beyond this, I work through queries from my clients that may include contract reviews, data analysis or third-party communication with Network Providers and Retailers.